Side Effects May Include Artificially Inflated EPS

Why a profitable pharma company buying back stock is usually telling on itself

You wake one morning from uneasy dreams and find yourself transformed in your bed into the CEO of a mid-cap publicly traded pharmaceutical conglomerate. Stranger things have happened.

There’s no time to dwell on it, because when you arrive at the office, your board of directors sits you down and asks a Very Important Question about where to direct the billions of dollars of free cash your company generated this year. They politely suggest four options:

Boost the R&D budget

Acquire a few promising biotech startups

Build additional manufacturing capacity

Buy back shares of the company

You ask your CFO about the last option, because it looks just a bit out of place.

“If you so wish,” the CFO explains, “we can acquire stock of the company at the market’s current value.”

“Why in the name of all that is holy would I want to do that?”

“Well, if you think we don’t have any better things to do with our money, we can just return cash to our shareholders.”

“Can’t we just do that through a dividend?”

“We could, though specific tax treatments and market mechanics make share repurchases a marginally more efficient vehicle for that distribution.”

“I see.”

“Oh, and by shrinking the denominator of our outstanding shares, your yearly salary package will automatically increase.”

You scratch your chin, pondering this profound ethical dilemma for approximately one second.

“Absolutely,” you say, slamming the table. “Let’s buy back some shares.”

Jokes aside, there is a standard hierarchy of reasons a pharma company buys back its own shares. Ranked roughly from most defensible to least, they look like this:

You have literally run out of things to do with the cash. Every research program you believe in is fully funded. The M&A targets you want are priced at insane multiples. A new manufacturing plant would sit half-idle. Your money has nowhere productive to go; so returning cash to investors is the correct move. (We will come back to how rarely this is actually the case.)

It’s a slightly more tax-efficient way to return that cash than a dividend. A dividend triggers a tax bill for every shareholder the moment it’s paid, whether they wanted the cash or not. A buyback, on the other hand, lets the shareholders who want out sell, lets everyone else defer, and converts the whole mess into capital gains rather than dividend income.

You’re mopping up dilution from stock comp. You pay your employees in company shares, so you buy back roughly that many shares on the open market to keep existing holders from getting watered down. Fine.

You think your own stock is cheap. If you absolutely believe the market is mispricing your future cash flows, buying your own stock is a sound value investment. This is a reasonable choice if you are right, and conveniently self-serving if you are wrong.

You want the EPS number to go up without the business improving. If you have fewer shares but the exact same earnings, your earnings-per-share goes up. It is a purely aesthetic change, like cutting a pizza into six slices instead of eight. Every slice is bigger, but that in itself does not create more pizza.

Your own pay is tied to that EPS or to the share price. If your company ties EPS to comp, a buyback (which flatters EPS) would make your yearly bonus bigger.

If you’ve read my piece from last month on the shape that pharma revenue takes, you’ll know it’s a highly portfolio-dependent business. That is, revenue from the portfolio is reliably positive-NPV, but individual products inside it are not. Some drugs are blockbusters that can pay for the whole campus; most, however, are flops that never recoup their trial costs. Such is the nature of an industry built on long-dated, heavy-tailed bets: it takes years to go from discovery to market, with plenty of binary clinical readouts in the interim, and a hard patent clock ticking on every winner from the day it launches.

Why do I bring this up? It is to say that, besides for the most defensible of reasons -- i.e. “We’ve run out of good things to do with the money!” -- it should almost never be logical to buy back stock. The business model of pharma is essentially funding lotto tickets with positive EV, and every drug you put into the clinic is another ticket.

Essentially, there is always somewhere productive for money to go in the pharma business. So when a profitable pharma company does big buybacks, especially near a high, with a patent cliff already visible on the calendar, it’s usually telling you one of two things. Either this company has outright stopped believing in the merits of its own R&D org, or the people running it are paid in a way that rewards a buyback today; and they won’t be around to care what happens in a decade.

If you don’t believe me, I have receipts.

Some Case Studies in Capital Allocation

Gilead

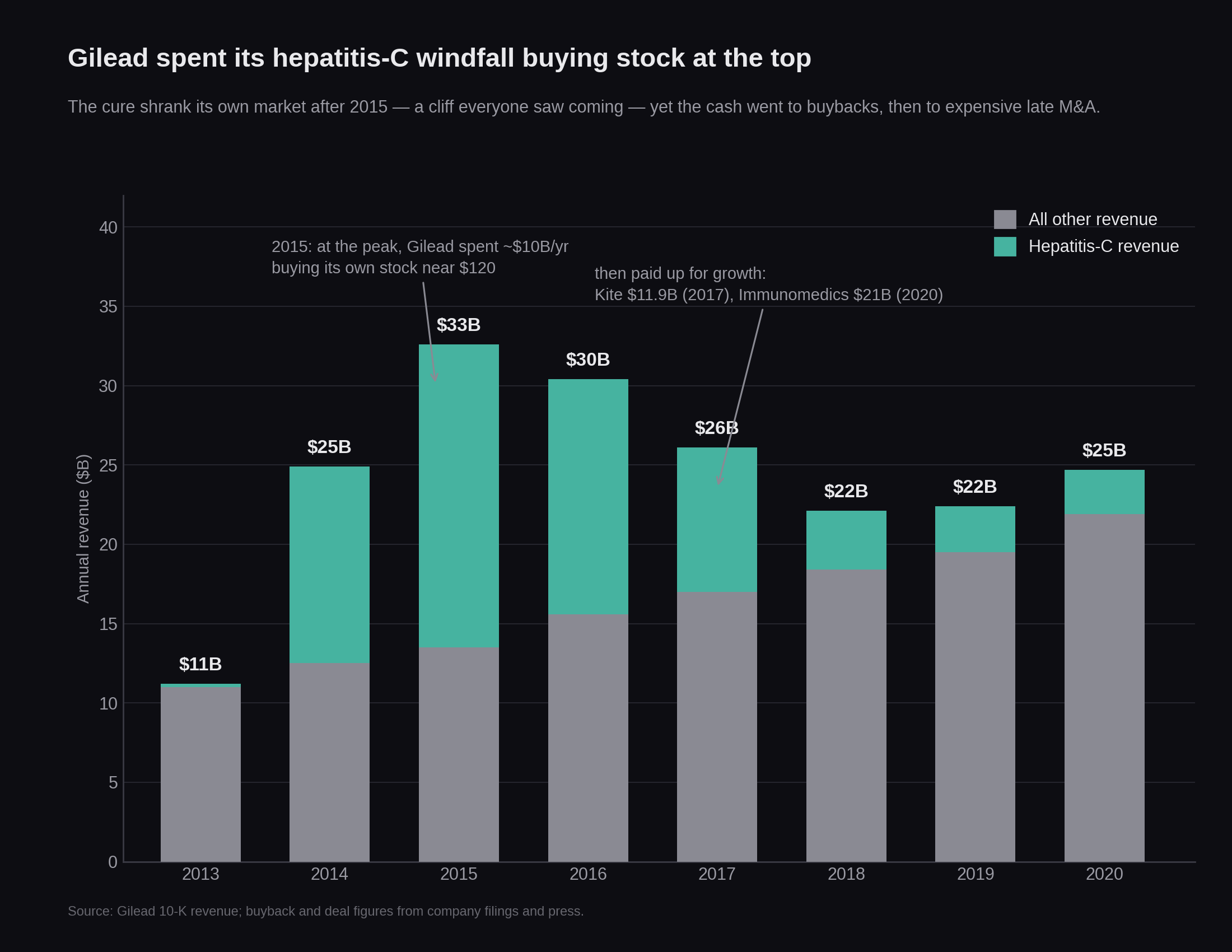

Gilead during the mid-2010s serves as an ideal natural experiment for a pharma that found itself with a dragon’s hoard of cash and no immediate plan for it. Their hepatitis-C drugs Sovaldi (2013) and Harvoni (2014) tripled the company’s revenue from $11 billion to about $32 billion in two years. At their peak, HCV sales were near $19 billion.

The catch was that these drugs actually cured the patients, meaning the total addressable market of patients was inherently deflationary. Sovaldi and Harvoni, effectively, were punished for their success. Everyone, including Gilead, could see the revenue cliff approaching.

How did they deploy this unprecedented windfall? By executing roughly $39 billion in share buybacks, of course. In 2016 alone, they spent $10 billion on buybacks -- mostly in the $90-$110 range, just off their all-time high of $120. By what I am sure is pure coincidence, CEO John Martin was paid almost entirely in stock. His reported 2014 package alone was around $193 million, and Reuters estimated his realized gains from 2009 to 2013 at somewhere in the $400 million range.

What’s hilarious is that Gilead said all of this out loud and without any shame at the time. Through 2016-17, while running ~$10B of buybacks, they sat on roughly $34 billion in cash while analysts begged them to buy literally anything else. Management’s official line was that they were “open-minded but disciplined.” Then-CEO John Milligan complained that every available asset was either “too early” or “too expensive,” even while admitting they desperately needed a deal to grow. They even poached an oncology head from Novartis to go shopping. Wall Street helpfully suggested Incyte, Tesaro, and Vertex. Gilead passed on all of them, deciding the best possible purchase was $39 billion of Gilead.

(To be fair, passing on Incyte aged rather well when their lead drug failed in 2018, dodging a $28 billion bullet. But that just proves the point, in my view: they seriously looked around and decided everything was too expensive, buying their own stock at the absolute top instead).

Then the cliff arrived exactly on schedule, and Gilead looked into their internal pipeline and found cobwebs. Panicking, they went on a shopping spree at a massive premium, buying Kite Pharma for $11.9 billion in 2017, striking a deal with Galapagos for $5 billion in 2019 (whose lead drug the FDA promptly rejected), and Immunomedics for $21 billion in 2020 (paying more than double its market cap from the week prior). Analysts screamed from the rooftops that they were overpaying. Meanwhile, hepatitis C revenue cratered from $19 billion to $4 billion, dragging total revenue back to $22 billion by 2018. About $100 billion of market value vanished into the ether between 2015 and 2018, and their stock languished in the $60s for years. As late as early 2021, Gilead was down 30% over the previous twelve months while the broader biotech ETF was up nearly 70%.

The punchline is that the exact same assets Gilead panic-bought at a premium in 2017 and 2020 already existed in 2015. They were right there, waiting to be bought, back when Gilead was busy purchasing its own stock at record highs.

Pfizer

Throughout the 2000s, Pfizer operated like a Katamari ball, growing via serial mega-acquisitions: Warner-Lambert ($90B) in 2000, Pharmacia ($56B) in 2003, and Wyeth ($68B) in 2009. Their main strategy for revenue growth during this period was buying other people’s blockbusters, milking them over their remaining patent life, all while its own internal productivity was fading.

Between 2009 and 2018, Pfizer distributed 114% of its net income and 167% of its R&D budget to shareholders. Under CEO Ian Read, buybacks ran at about three times what Pfizer was setting aside for US federal taxes, even as Read complained publicly that the US tax code had the company fighting “with one hand tied behind our back.”

What did these decades of frantic buybacks achieve? A stock that went essentially nowhere. In 2019, Pfizer’s share price was still below its 1999 high. They had successfully transformed themselves into a high-yield bond that happened to own some intellectual property.

Amgen

From 2009 to 20181, Amgen spent $47 billion on buybacks -- around 131% of its R&D budget. Much of this was debt-funded. They were issuing bonds domestically while parking cash overseas to game the tax code. During this era, Amgen’s adjusted EPS soared from $5 to $12.58. This growth was driven almost entirely by a shrinking share count and aggressive price hikes on older drugs like Enbrel, rather than the invention of new medicines.

And it... worked? Amgen’s stock roughly tripled between 2011 and 2018. However, with organic growth thin and biosimilars closing in on its aging blockbusters, Amgen eventually had to go out and buy growth that it had neglected to build --Otezla @ $13.4B in 2019, Horizon Therapeutics @ $27.8B in 2023 -- both at handsome acquisition premiums.

Today, Amgen carries around $60B of debt on their books. So while buybacks bought a higher EPS and several good years, the reinvestments it was deferring eventually came due with a painful markup. This kind of deferral, in my view, is what makes share buybacks seductive to anyone working a ~5-year comp horizon: they can paper over stagnation for long enough to get paid well... long before karma kicks in.

Teva

Eli Hurvitz, a one-of-a-kind pharma CEO who I wrote at length about last year, built Teva brick by brick on patient, opportunistic dealmaking and one real innovation asset: Copaxone, which at its peak was yielding Teva more than $3B a year and a huge slice of profits. Hurvitz’s next few successors, however, managed to reverse his life’s work in record time.

By the early 2010s, with Copaxone’s major patents already lapsing and generics on the doorstep, Teva authorized a $3B buyback in 2011, kept paying a fat dividend all throughout, and then spent $40.5B on Allergan’s Actavis generics unit in 2016 -- at the very top of the generic-pricing cycle, taking on around $35B (!!) of debt to do so. Teva basically handed cash back to shareholders and levered up for a low-margin commodity business at the precise moment its highest-margin franchise was falling off a cliff and its branded pipeline was bare.

Then US generic prices blew up overnight as the FDA sped up generics approvals, and Teva’s stock did a Kingda Ka; going from about $70 in 2015 to roughly $8 in 2019. Their dividend was cut; cut again; and then finally suspended in December 2017 alongside 14,000 job cuts (and all of this was before opioid and price-fixing litigation showed up, but that’s a whole other story).

The tragedy of Teva is worth introspecting about. It shows us that failure isn’t really about buyback mechanisms at all: during these bad years, poor decision making wrecked the company; regardless of whether its cash was leaving as repurchases, dividends, or a catastrophically mistimed acquisition.

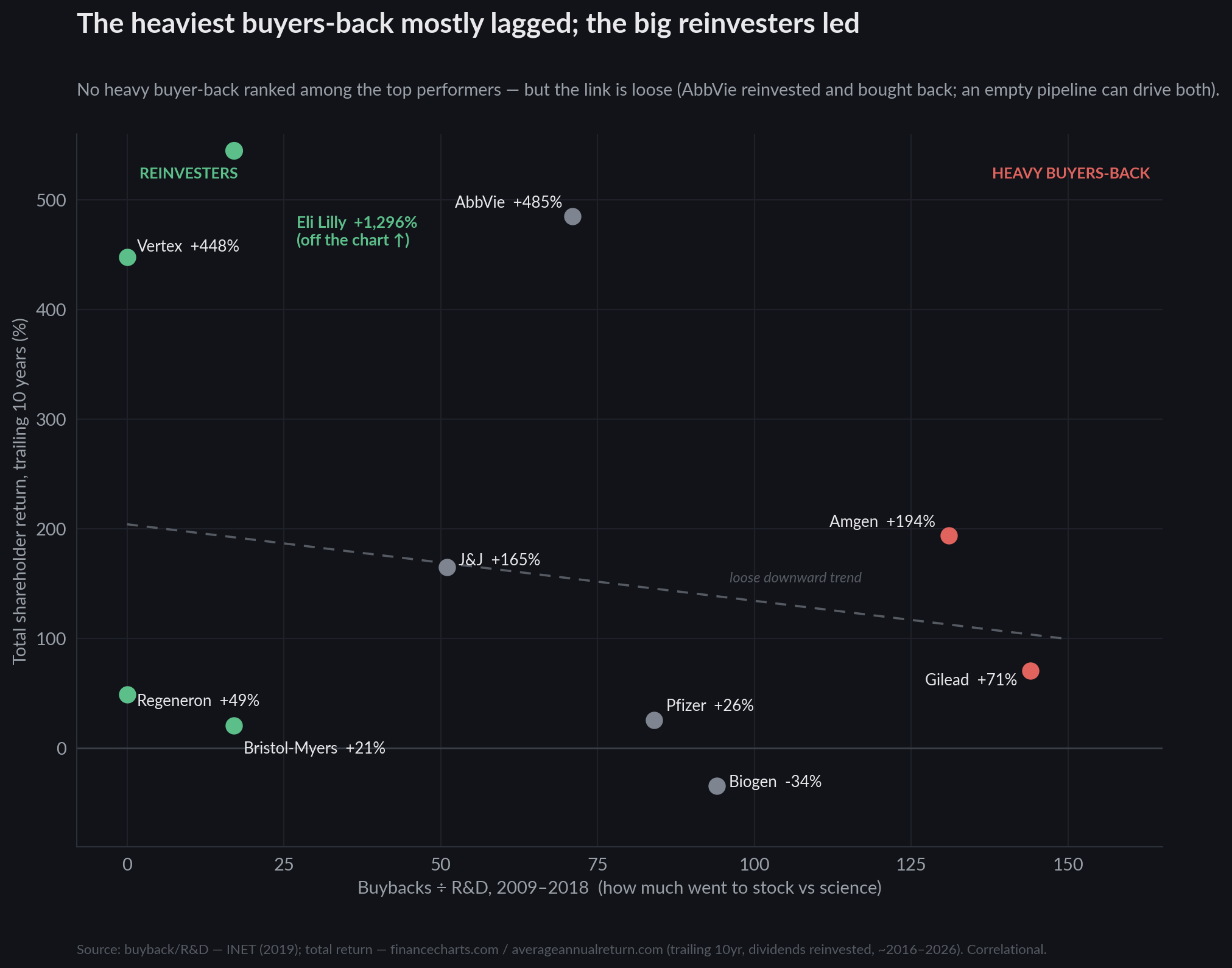

The control group

A few companies faced an identical expensive-acquisition market over this same 2009-2018 window, but made the opposite choice as the companies above.

Regeneron, for instance, did $0 of buybacks and $0 of dividends, and spent $12B on R&D against $6B of net income; reinvesting a large share of its profits into its own labs! All the while it was one of the best-performing large-cap drug stocks of the decade. Vertex too did $0 of buybacks, ran R&D at around 70% of revenue, and built its cystic-fibrosis franchise in-house; it compounded prodigiously. And today’s beloved Eli Lilly was spending just $9B on buybacks against $52B of R&D -- a 17% ratio, among the lowest in big pharma -- and ended up printing out tirzepatide, which came from an internal R&D effort.

And these CEOs were still well paid! Regeneron’s Leonard Schleifer and George Yancopoulos sat at the top of the pharma pay tables for years (Yancopoulos hit $268M in 2017, ~99% of it stock). So both the buyback-heavy crowd and the reinvesting crowd had richly paid, stock-incentivized leadership.

Steelmanning Share Buybacks

I’ve been writing as if stock buybacks are a vampiric curse that inevitably drains these companies. The actual data is slightly more annoying to my thesis, so let’s steelman the opposing view.

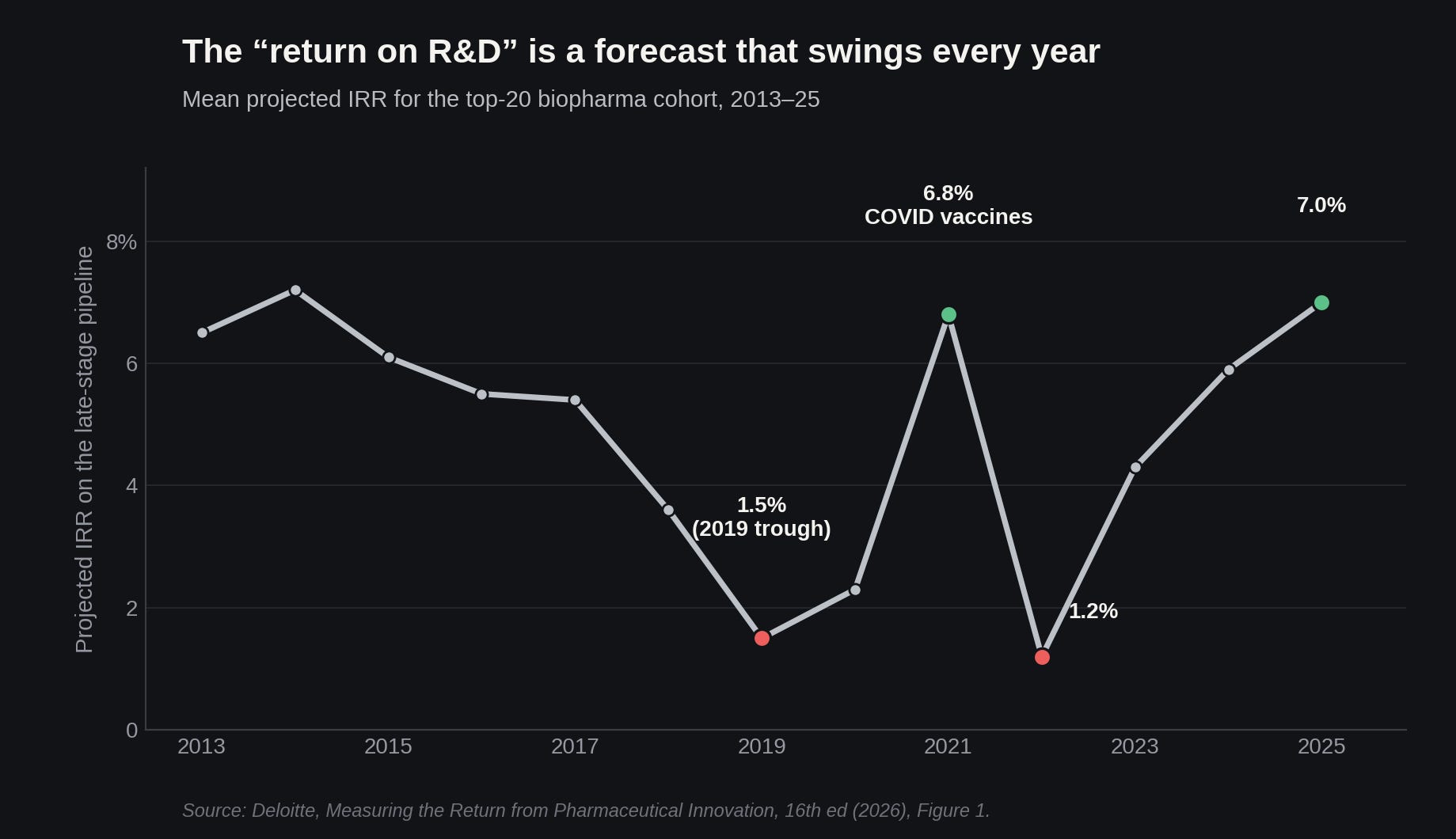

Over this exact window, pharma R&D returns evaporated. Deloitte’s running study of the large-cap drugmakers put projected IRR on late-stage R&D at just over 10% in 2010 and around 1.5% by 2019 -- close to a linear decline across the decade. If your own labs are returning a couple of percent against a higher cost of capital, “the money has somewhere productive to go” stops being a law of nature and starts being a hilarious delusion. Instead, it has to be checked company by company. For some firms in some years, reinvestment really was the worse bet, and handing cash back so shareholders could go buy index funds was the only defensible call.

And causation often runs backwards from how I’ve framed it, too. A thin pipeline is usually the disease; the buyback is the visible symptom. The company with nothing worth funding does buybacks because it has nothing worth funding -- and it’s the empty pipeline, not the repurchase, that eventually starves the business. Amgen makes the same point from the other direction -- its buybacks paid off handsomely for years, before the bill came due.

Countering the steelman

That is the strongest version of the counterargument, from what I can tell. Unfortunately, it also has two rather squishy soft spots.

First, consider what an “internal rate of return” metric actually captures. It functions almost entirely as a forward-looking projection based on analysts guessing at peak-sales estimates, heavily seasoned with probability-of-success multipliers for whatever late-stage assets a company already happens to own. Furthermore, assets mysteriously vanish from the sample the exact moment they actually launch! The metric therefore describes the hypothetical paper “productivity” of current late-stage projects, while providing precisely zero information about the expected return on the marginal dollar of new investment… which, inconveniently for us, is the exact variable a buyback decision actually relies upon.

We must also recognize that the 2010s’ 1.5% era ROI represents a cyclical trough! After the R&D doldrums of those years, the metric has since climbed to a much more cheerful 7% in 2025. Yes, while it’s true that stripping GLP-1 assets2 out of last year’s model drops the return back to around 4%… nobody ought to be surprised that this industry’s aggregate returns are basically tethered to a baseline forecast, while being violently dragged upward by a tiny cluster of massive lottery-ticket successes. If anything, it should suggest to the reality that the total R&D ROI number is an average across an enormous range of company-specific ROIC over a given period; with about as much fidelity as “average temperature of Buenos Aires for 2025.

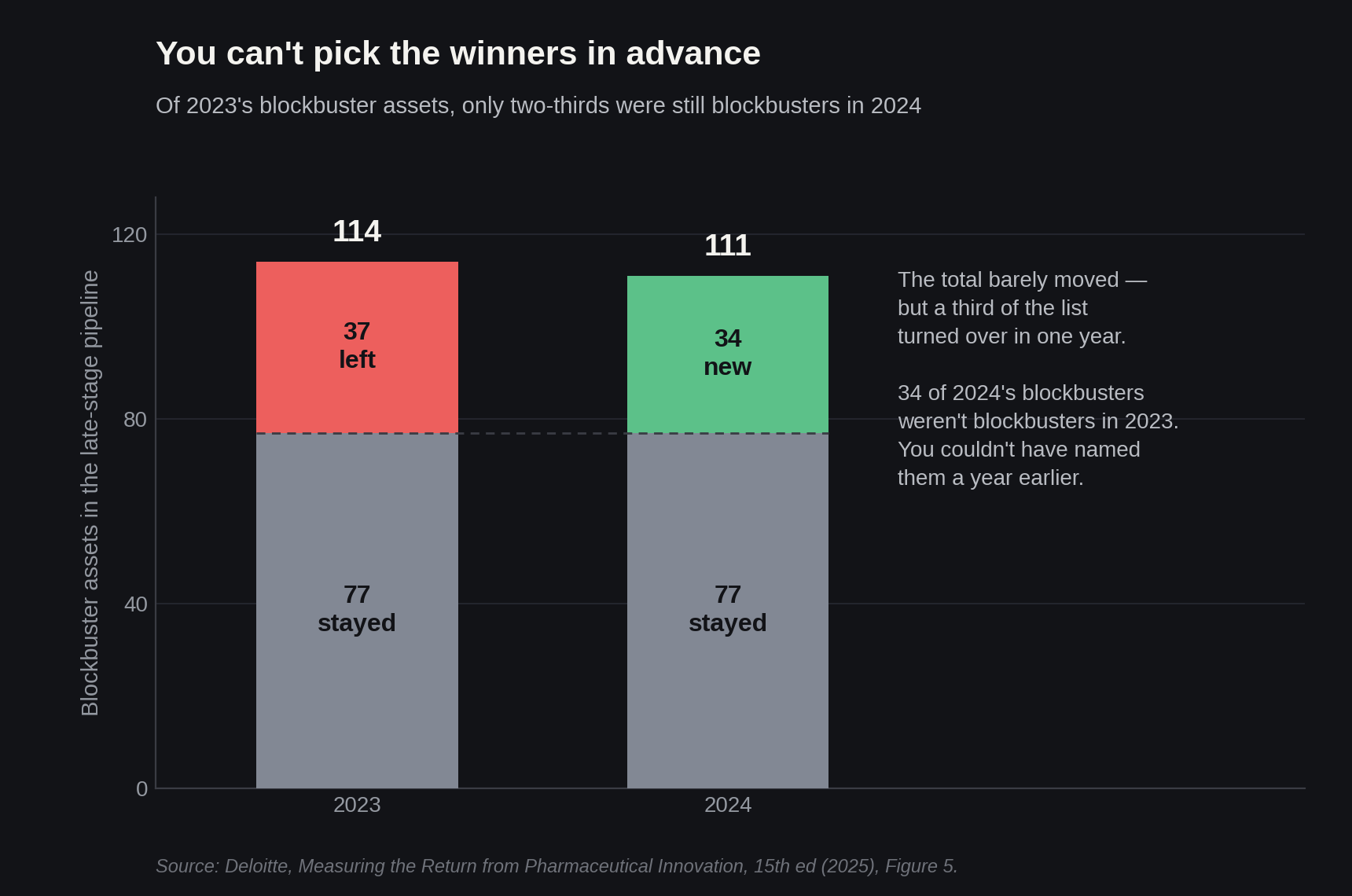

This structural distortion explains why industry averages are practically useless for resolving the core capital allocation question we’ve been circling around in this essay. A general, sector-wide decline in research productivity operates completely independently from whether one specific company - sitting on a specific dragon's hoard of cash - actually lacks productive investment opportunities; sure, a clever skeptic might retreat to a marginalist argument here, suggesting that pharmaceutical companies obviously fund their most promising ideas first, meaning any additional cash inevitably flows toward lower-quality, bottom-of-the-barrel projects deeper in the pipeline. But that marginalist framework secretly launders a very silly assumption: that pharmaceutical companies can accurately rank their projects in advance (spoiler: they cannot). This, infamously, is a capability the pharma industry demonstrably lacks.

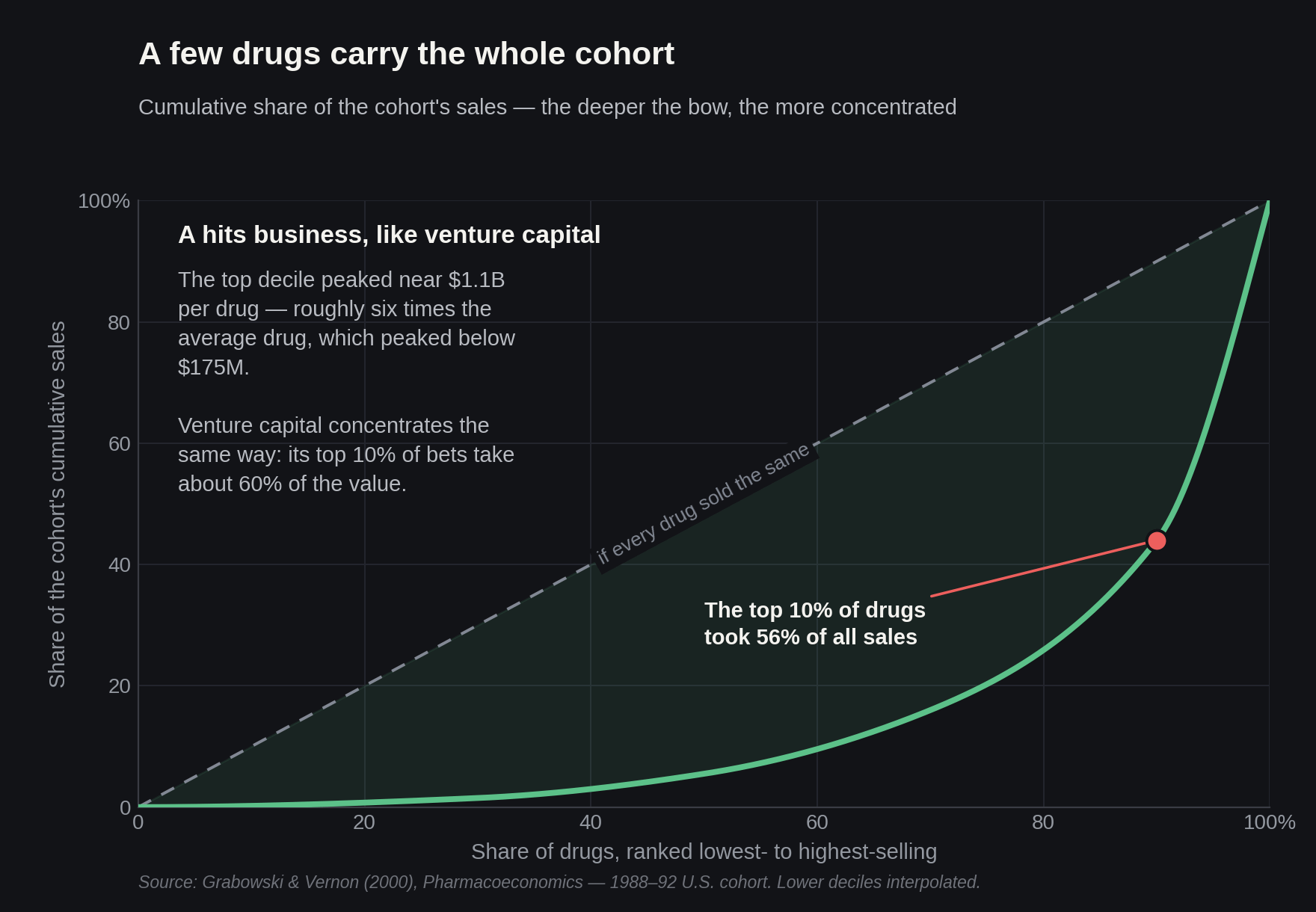

And from what I can tell, the long-term empirical data on this pretty much seals the case. If you look at Grabowski's research on pharma R&D returns, you find a classic power law distribution; that is to say, the top decile of drugs generates roughly half of the sector's total lifetime value. Deloitte's latest estimate of pipeline ROI agrees; suggesting about 9% of assets account for a staggering 70% of projected sales. Since these extreme mega-blockbusters refuse to identify themselves until their clinical trials actually read out - the exercise of trying to guess Whether Your Next R&D Dollar Yields Diminishing Returns or Not requires epistemic superpowers that literally nobody possesses.

So, fine: I am willing to bite the bullet on the most modest version of this argument. Industry-wide R&D returns really did look pretty dismal through the 2010s! And if a pharmaceutical company was staring into the abyss of an empty pipeline, and every acquisition target was priced like a small sovereign nation - a stock buyback could theoretically be a mathematically defensible move. But my charity runs out the moment we try to apply this smoothed-out industry average to something like Gilead’s set of specific galaxy-brained portfolio decisions when they found themselves with a Hep-C revenue sized war chest. Just to hammer it in one more time: they sat on a enormous pile of $34 billion in cash; told analysts they were shopping; simulataneously called every target too expensive -- and then bought their own stock near an all-time high with a scheduled patent cliff already on the calendar. That was purely bad allocation on the company’s own stated terms.

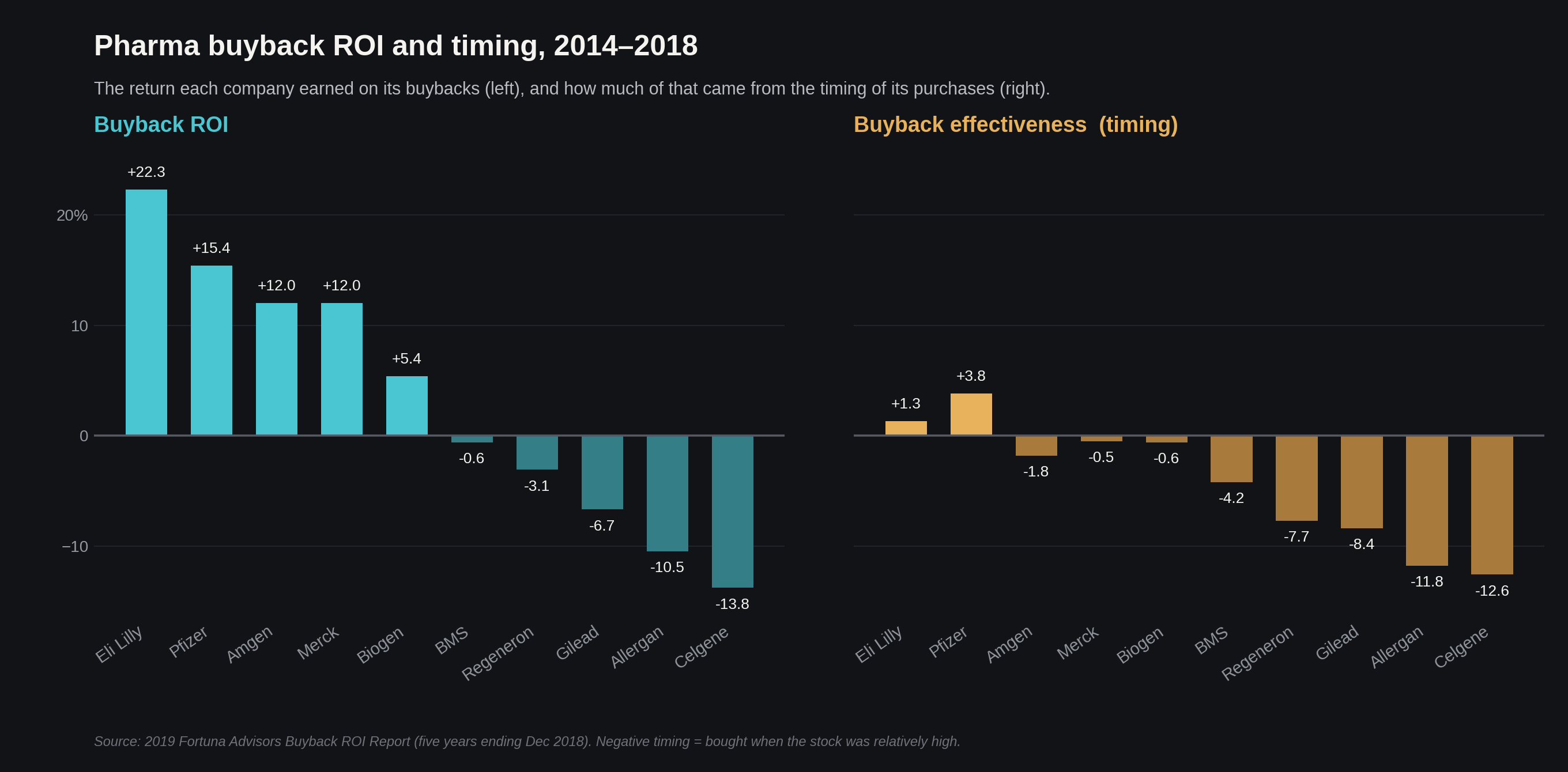

Lucky for Gilead, they have plenty of company on the Naughty List. A 2019 Fortuna Advisors study found that 64% of the S&P 500’s largest repurchasers bought most heavily when their own shares were relatively expensive -- paying up near the highs. As Deutsche Bank’s global head of macro, Jim Reid, said last year: “Buybacks tend to occur more at market tops than bottoms...companies often buy high, not low”. A long-horizon owner staring at a visible cliff keeps the powder dry and then buys the dip. Gilead, however, blew their cash at the absolute peak instead, and then scrambled to refill their coffers just as the stock became cheap again.

Back in the Chair

Alright, CEO. The board is waiting. You have four options -- three of them put money back into the lottery that this whole business runs on, and one takes money off the table.

Taking money off the table is the correct choice exactly when the first condition is met: every program is funded, all external assets are overpriced, and your company’s cash has nowhere better to go. Sometimes that is true! But in a business built on positive EV, it usually isn’t. And the cases above are what it looks like when a management team talked itself into “yes” anyway, usually right around the time its own stock-based pay was vesting.

So before you slam the table and demand a buyback, ask yourself: is everything I would want to back already fully funded? Is that biotech startup actually overpriced, or does it just look expensive compared to my artificially inflated EPS?

If your honest answer is that the money has somewhere productive to go, then send it there. The universe does not care about your year-end bonus, but it might occasionally reward you for inventing a medicine.

Decade figures (2009-2018): Lazonick, Tulum & Hopkins, "Financialization of the U.S. Pharmaceutical Industry," INET, 2019.

(This, by the way, prompted Deloitte to title their most recent edition of their annual report on pharma innovation “Navigating the GLP-1 boom.”)