China has caught up in biotech. How screwed are we?

On July 19th, Yoni Ben-Shimon and I are hosting a half-day Bay Area retreat to dig into the ideas in this piece. We’re bringing together biotech operators and policy people. If that's you, apply here.

If you have successfully avoided Biotech Twitter recently, congratulations: you’ve been missing out on the collective realization that we are all doomed. Every other day, it feels like another Chinese company out-licenses an asset to a Western pharma for a headline number with an offensive amount of 0s, and my feed immediately fractures into people demanding everything from “total embargo!” to people pointing out that “well, akshually, it might be far too late already”.

A company launch announcement a few weeks ago brought this low-level panic to a boil when RA Capital announced they had backed Serapha. Serapha is a base-editing spinout of the Chinese biotech YolTech, and it may or may not be heavily borrowing its homework from David Liu’s lab at Harvard (disclaimer: this is hearsay, and I am not a lawyer). This news predictably generated a lot of heated debate, with pointed to and fro in every possible direction. We must collaborate! We must ban! We must reform! We must go to China and see for ourselves!

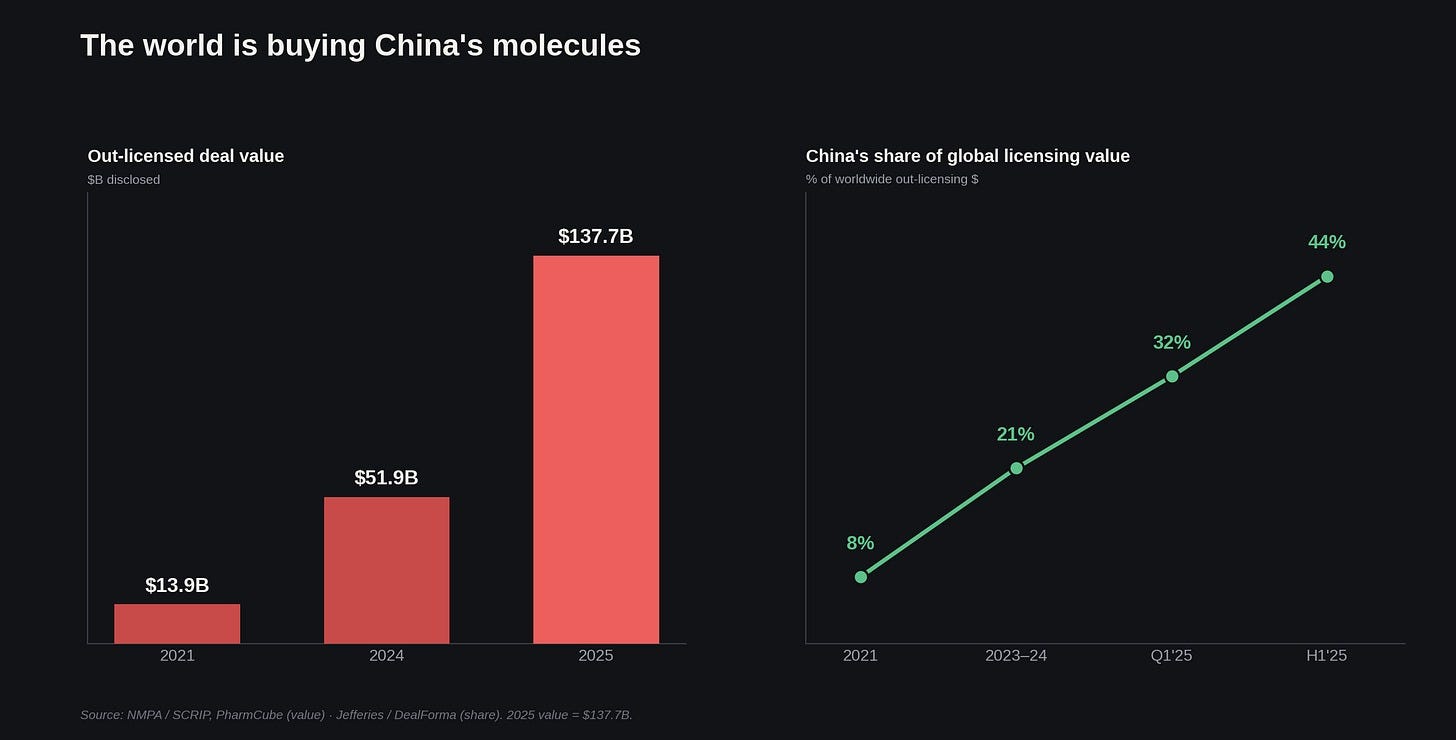

The numbers underlying this panic are, unfortunately… actually worth worrying about. Chinese companies out-licensed $137.7 billion in drug assets last year, which is somewhere between three and ten times the 2021 level depending on how charitably you categorize milestone payments. Two Septembers ago (and what feels like a lifetime away now), Akeso’s ivonescimab became the first drug to beat Keytruda head-to-head in lung cancer. If you have been tracking the sheer volume of US-China deal flow since that data dropped, you might reasonably conclude that it is time to start studying Mandarin.

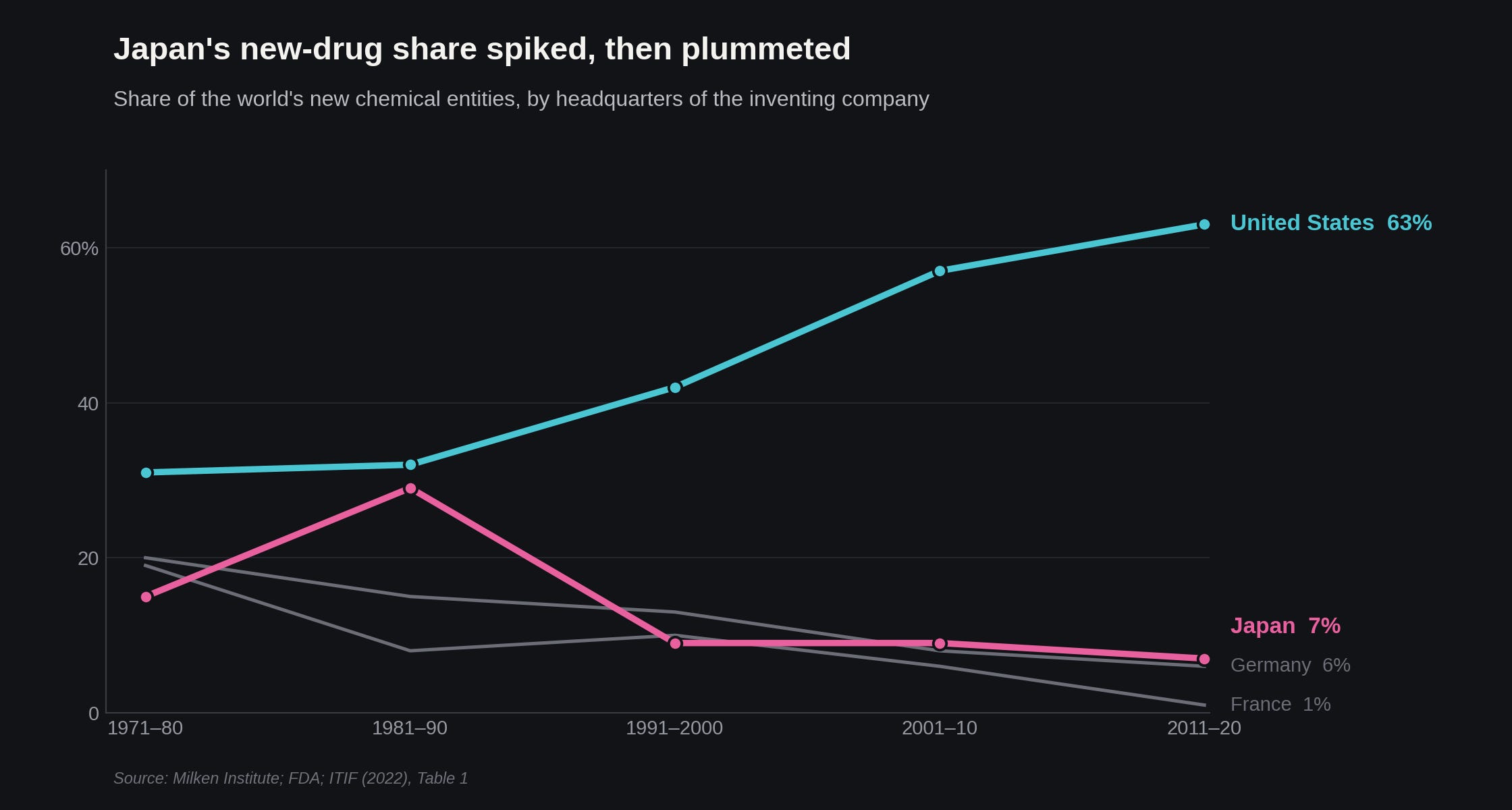

But before you do, there is some historical precedent that suggests we should perhaps take a deep breath. In 1985, Science ran a piece titled “Biotechnology in Pharmaceuticals: The Japanese Challenge”, with the same kind of alarmist “are we screwed” sentiment many are feeling today.

That 1980s panic rested on two true premises. First, Japan had rapidly taken over a huge chunk of medical manufacturing; Companies like Ajinomoto, Kyowa Hakko, and Takeda possessed the best industrial fermentation technology in the world. This was a massive advantage because the hot new field of that era was biologics, which required brewing in giant bioreactors. Second, the capital-S State had stood firmly behind it: Japan’s then all-powerful governing body, MITI, had declared 1981 “The Year of Biotechnology” -- feeding the sector into the same industrial woodchipper that had already consumed American steel, autos, and chips.

And yet, despite all of that buzz, Japan’s share of new chemical entities over the next three decades plummeted from 29% to 7%.

I bring up this precedent because Japan in 1985 held the same hand of cards China is holding right now, plus one that China is still missing. Japan made the drugs, the state was subsidizing the effort, and on top of that they had a real basic-science engine with a track record of first-in-class drugs -- the first statins (Sankyo), the first PD-1 antibody (Ono), and the first IL-6 antibody (Chugai). Japan brought more to the table than China has managed to assemble, and it still lost, because it never built the commercial machine that carries a molecule to a global launch. The US still holds that as an ace up its sleeve.

Or maybe not. If China has truly caught up, the open question is which historical disaster this will actually rhyme with for America’s place in making new medicines. Will China mirror Japan, failing to translate manufacturing dominance into innovation? Or will the US mirror mid-century Europe, which possessed the world's best basic science and R&D infrastructure but eventually lost its leadership position anyway? From what I can tell, the answer turns on a barbell. Yes, China has built an absolutely formidable position in the middle of the drug-development stack -- the long, grueling stretch between a known biological target and an approved, scaled product -- and that is kind of terrifying. And yet at the two extremes, the West is still happily ahead: we still have a commanding lead in discovering paradigm-generating basic science, and the commercial machine that turns an that cool science into a global money-printer. Whether China’s bulging middle is enough depends entirely on whether those two ends can evade capture.

If that is what you already knew, great, you can click off now and have a wonderful day. If you are not satisfied by that answer, because things are never actually that simple, please read along.

I wrote the rest of this piece because I suspect very few people know where the data on China’s current position actually lands, and I wanted to look at the numbers myself rather than absorbing them via angry quote-tweets. Last year, I traced the structural shifts within China that built up to this current moment -- from their regulatory overhauls of the NMPA to a post-Covid capital crunch. This chapter picks up where that history leaves off, trying to figure out exactly what kind of fortress China has managed to build since.

Let us start with the middle then, shall we?

The world is buying China’s molecules

The best place to begin is probably the numbers surrounding deal flow and the sheer amount of capital changing hands. Last year’s $137.7 billion in out-licensed assets pushed China’s share of global out-licensing value to a staggering 44% for the entirety of 2025—a dominating momentum that has carried straight into 2026.

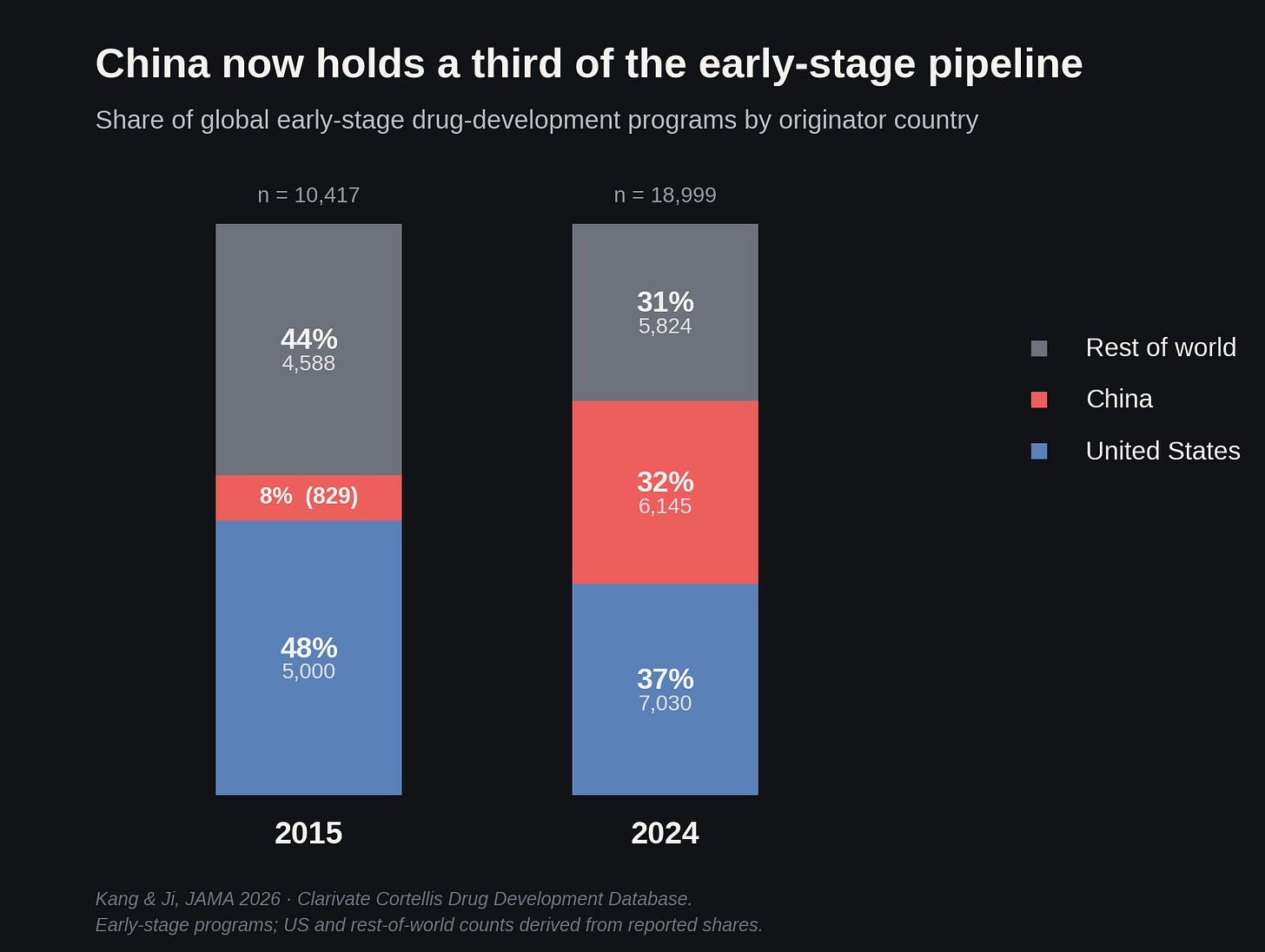

If you look at the composition of the global clinical pipeline today, about a third of it now originates in China. Back in what feels like the ancient history of 2015, Chinese-origin programs were a mere 8% of early-stage development; meanwhile, the US was sitting comfortably at 48%, the rest of the world at 44%. But by 2024, China was at 32%, the US had slipped to 37%, and the rest of the world to 31%.

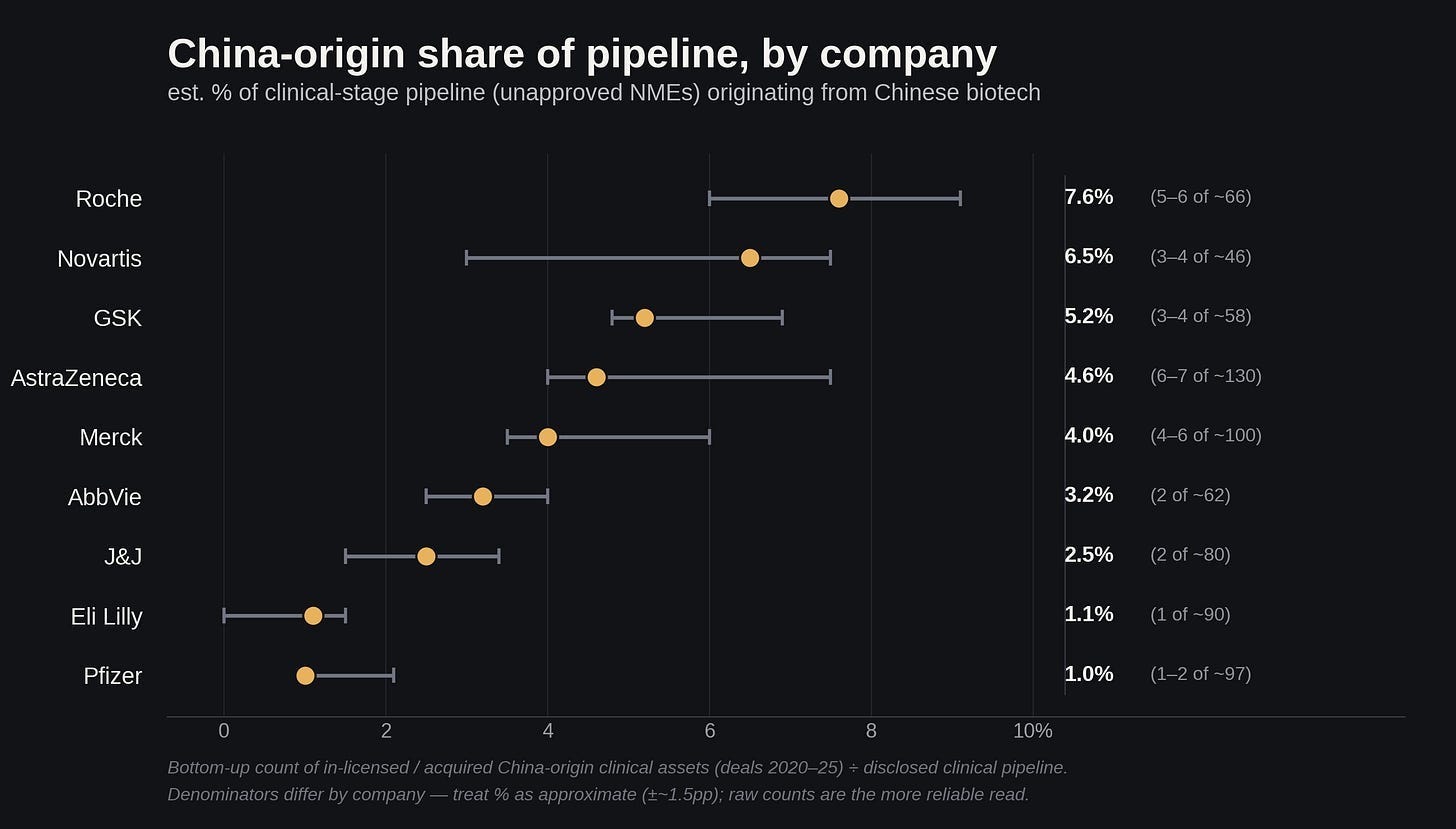

The weird part is where these programs actually end up. Many programs are now parked within established Western portfolios, rather than staying at strictly Chinese companies. They’re right under our noses! Across the big pharmas, China-origin assets now make up about 5% of their clinical pipeline -- with Roche highest at about 7.6%, then Novartis near 6.5%, GSK around 5.2%, AstraZeneca 4.6%, and Merck 4.0%, trailing off to Lilly and Pfizer near 1%.

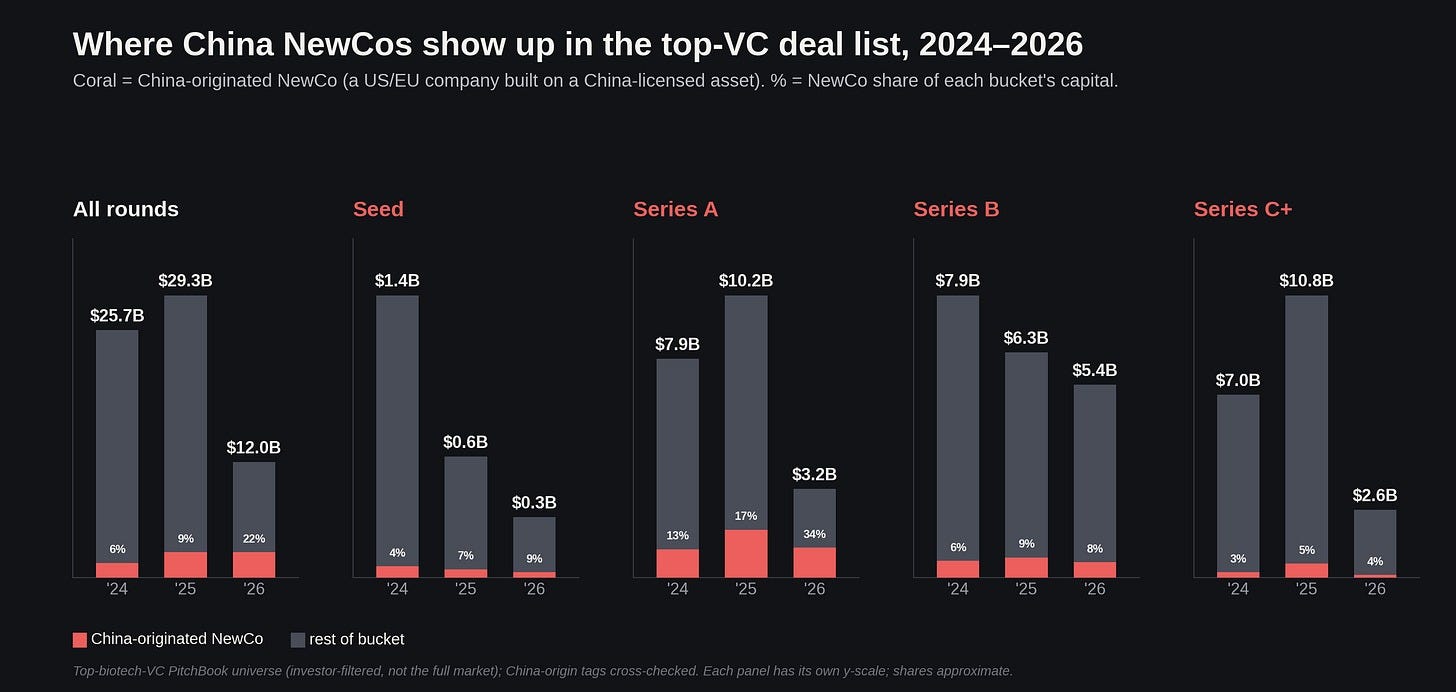

But of course, it is no longer just big pharmas turning Chinese by pipeline. US biotech venture money is now increasingly being deployed to spin out China-originated assets into brand new Western corporate entities -- “NewCos,” which are essentially American/European shells built entirely around a single, highly valued China-licensed asset. By capital, these NewCos have captured more than a third of Series A dollars in 2026 to date.

You may have even heard some of the names spawned by this model: Kailera (ex-Hengrui incretins), Verdiva (ex-Sciwind incretins), Avenzo (ex-Allorion/DualityBio/VelaVigo oncology), Candid (autoimmune T-cell engagers), Ouro (ex-KeyMed BCMA, since swallowed by Gilead); they are raising legit, non-trivial sized rounds from the likes of Bain Capital, Atlas Venture, and a lengthening list of blue-chip firms. This strongly suggests that institutional confidence in the asset-transfer model is beginning to harden into a kind of Corporate Conventional Wisdom.

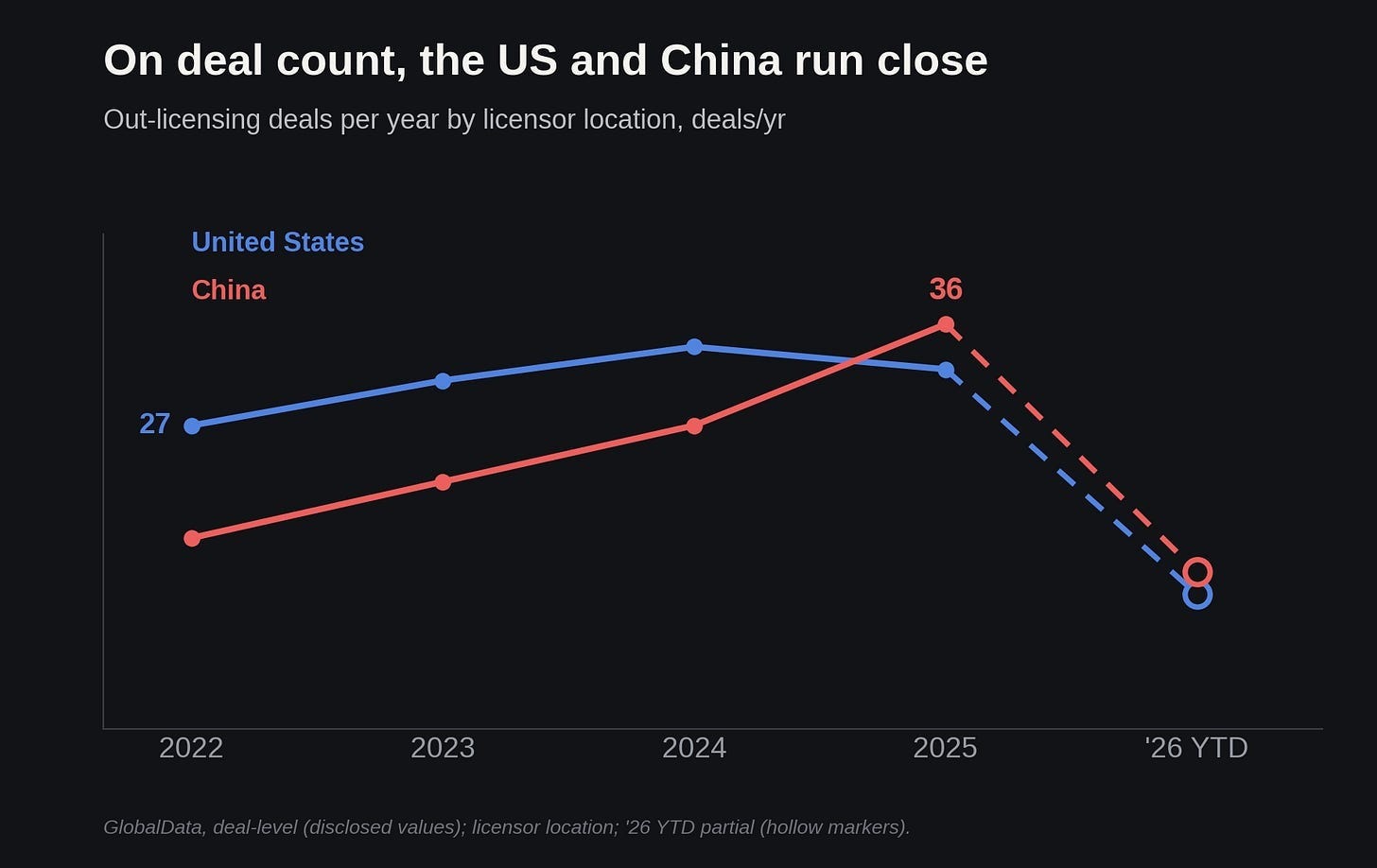

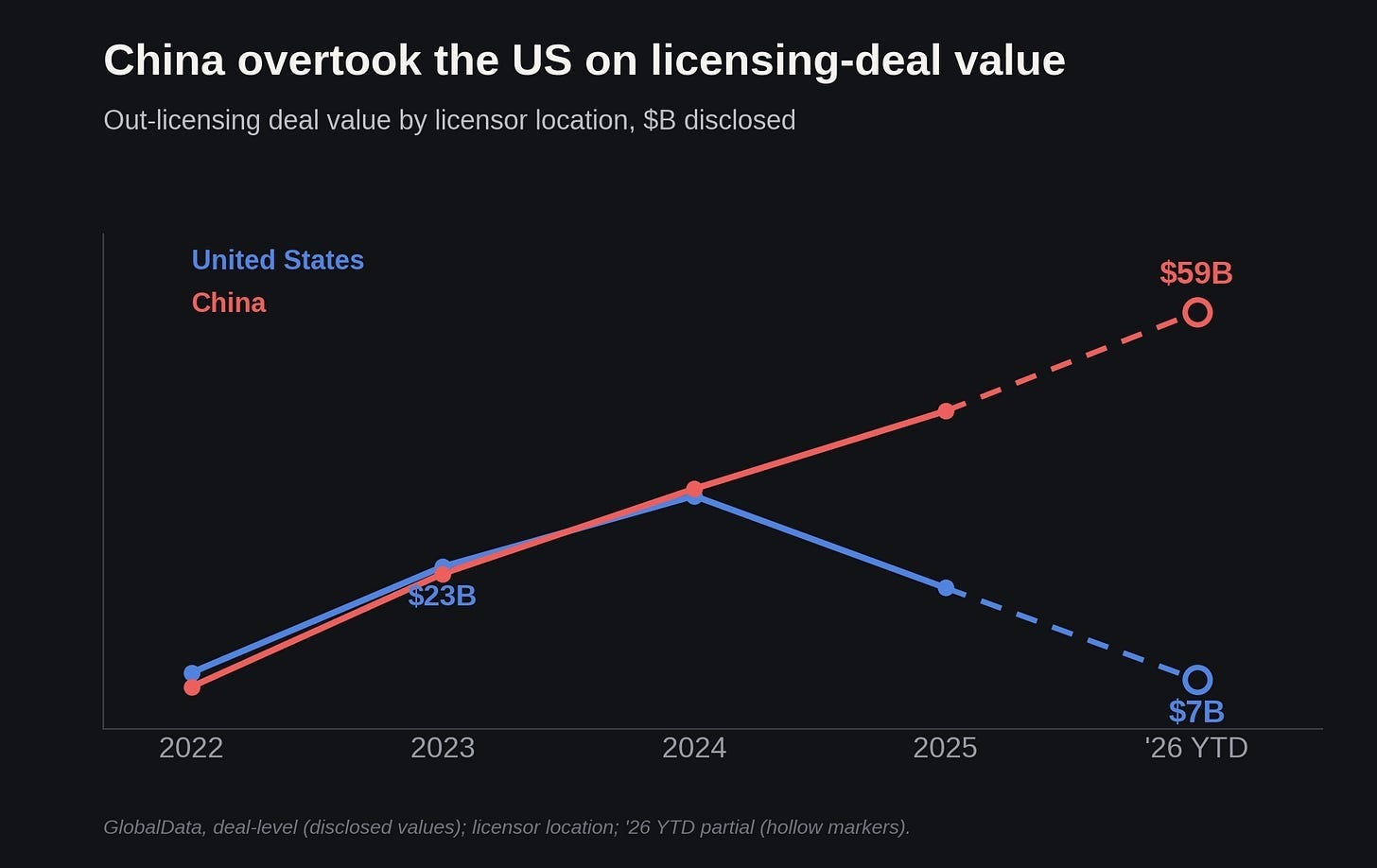

On pure deal count, the US and China have been running close for a number of years now, often trading places -- there were 27 US deals in 2022, with China catching up and jumping past the US to 36 in 2025. But Chinese deals are far bigger: so on total value, China has pulled quite decisively ahead, moving from a dead heat around $23 billion each in 2022 to China leading on pure dollars today. (I will come back to why the Chinese deals are so absurdly large later).

Where China already has us beat

Finances are one thing. But before we get to what kinds of therapeutic programs are actually being churned out, we should probably start with the domain where China has already led for a long time: making the physical stuff.

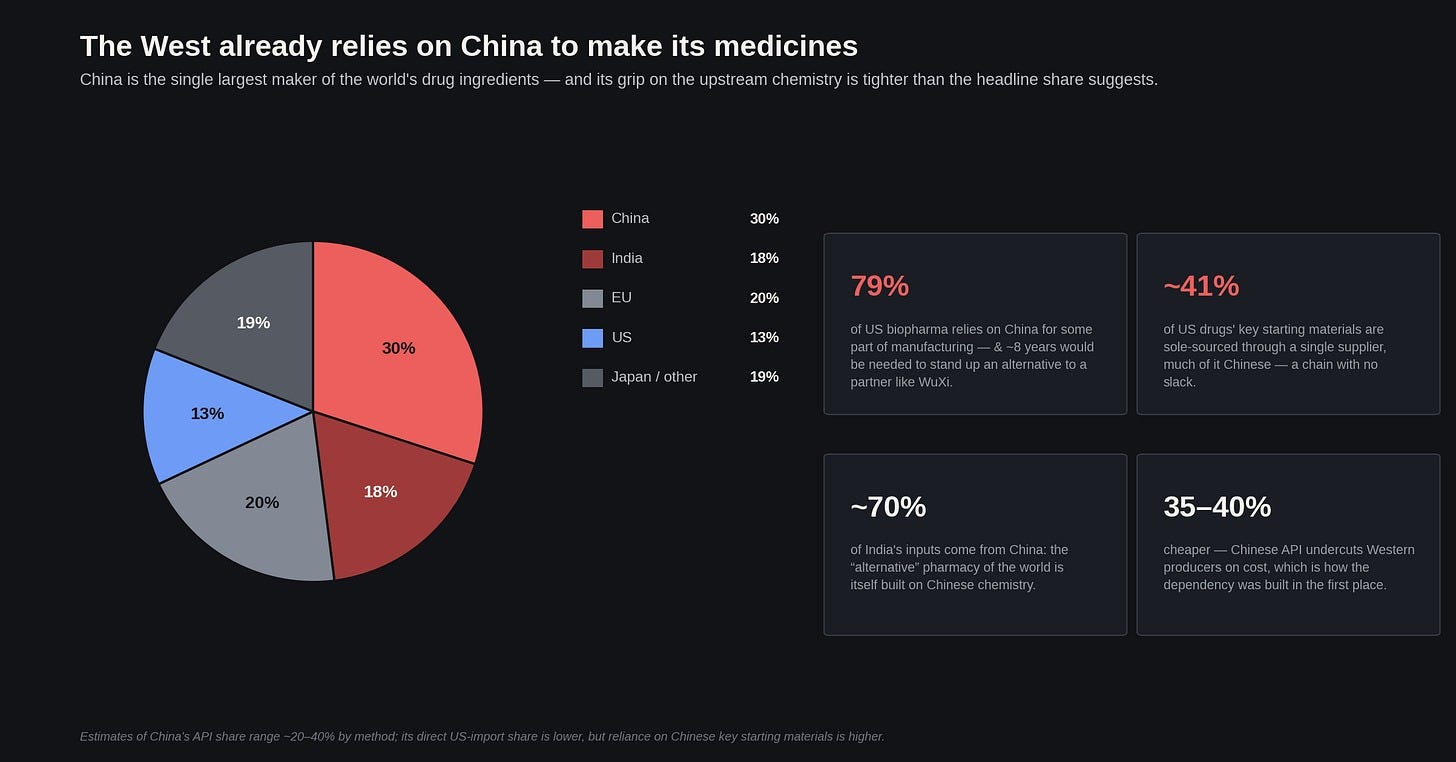

China, without question, absolutely dominates the global supply of active pharmaceutical ingredients. About 79% of the US biopharma sector relies on China for some part of its manufacturing. Roughly 41% of the key starting materials for US drugs are sole-sourced, coming from a single country, which is almost always China. Even India, frequently cited as the plucky alternative pharmacy of the world, relies on Chinese inputs for about 70% of its raw materials.

This dependency is a function of cold, hard, basic industrial economics. Chinese API is able to undercut Western producers by 35-40%, simply squeezing these competitors out on price alone. This is China’s specialty: state-subsidized overcapacity. Cheap loans and subsidized land let domestic producers run at a price point Western firms literally cannot match without going bankrupt.

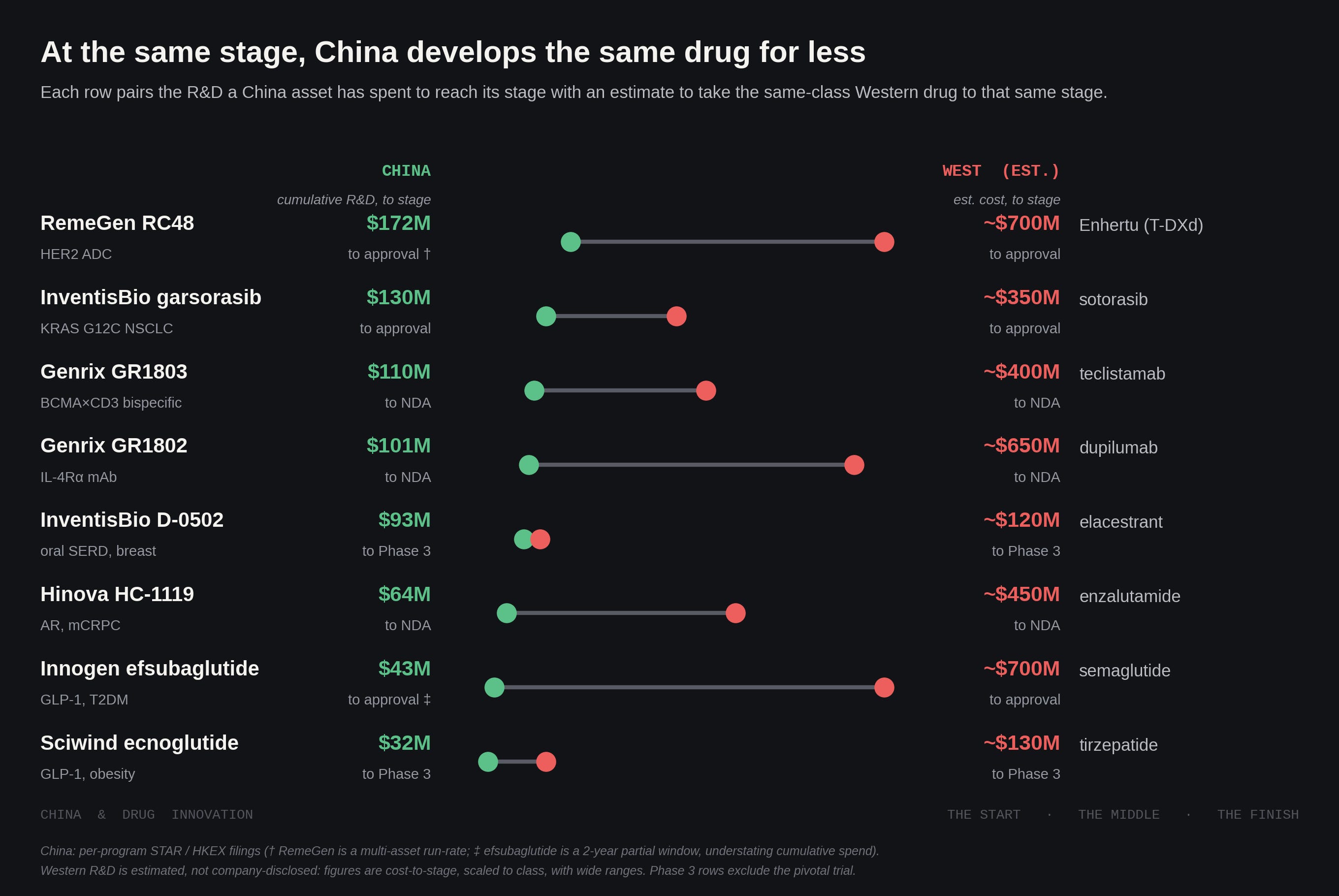

Naturally, this cost advantage is advancing past raw manufacturing and bleeding into the actual drug development process. Western companies are quickly learning exactly how cheap it is to push a drug through early-stage trials in China; after a few hours pulling R&D figures off financial documents from Chinese biotechs publicly listed on the Hong Kong and Shanghai exchanges1, I came out both enlightened and disturbed: a company called RemeGen took its HER2 ADC, RC48, to approval on about $172 million, against an estimated ~$700 million I benchmarked for Enhertu. Another, InventisBio, reached approval on its KRAS G12C inhibitor garsorasib for roughly $130 million, whereas its Western predecessor sotorasib ran an estimated ~$350 million. Chongqing based Genrix filed an NDA for GR1802, an IL-4Rα antibody, on about $101 million, against what I estimate as Regeneron’s ~$650 million to reach the same stage with dupilumab. Sciwind moved its GLP-1 obesity drug ecnoglutide into Phase 3 on roughly $30 million, versus the ~$130 million it took Lilly to get tirzepatide there.

If you assume an uncapitalized cost of roughly $300 to $500 million to run similar, successful clinical programs in the West, we are looking -- at the very least -- a massive two-to-threefold discount. And the drop-off is steeper still in early-stage development, which is where most programs actually live and die. It's simply impossible to deny the economics here, if you’re a pharma or a fund: if you want to run a lot of shots on goal cheaply and fast, China today is objectively the best place in the world to do it.

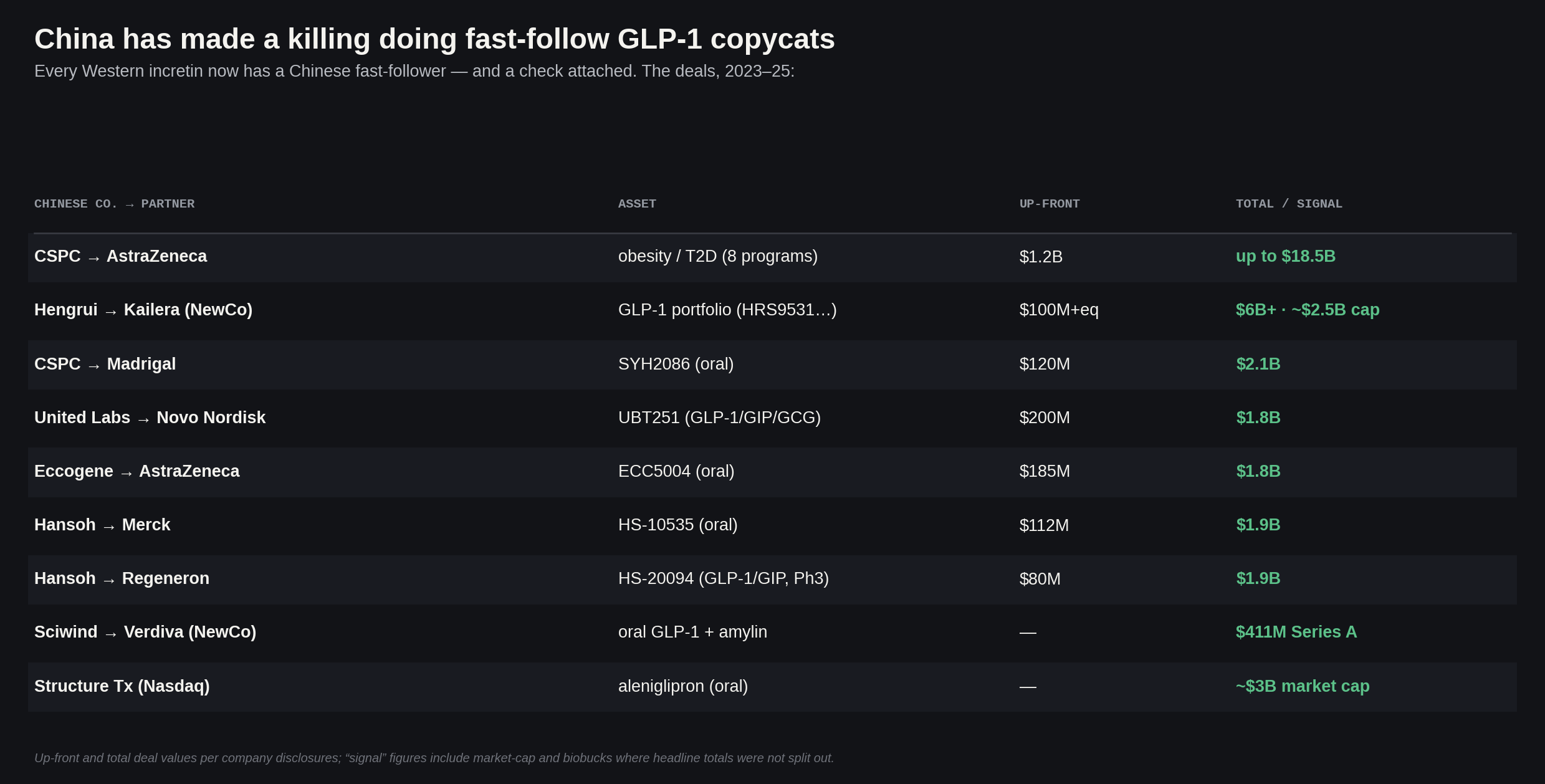

Leveraging that cost structure, Chinese firms are running a highly effective fast-follower strategy against the most profitable drug classes on the market. Take GLP-1s for example. Given the sheer market size generated by Novo and Lilly, obesity has become the ideal battleground for Chinese companies to swarm and fight over. So now nearly every major Western incretin program faces a rapidly developed Chinese alternative; Hengrui’s HRS9531, a GLP-1/GIP dual agonist, has started a 9,000-plus-patient cardiovascular outcomes trial, which is the kind of massive undertaking once run almost exclusively by Western giants. And according to my math, across roughly seven GLP-1 licensing deals since 2023 -- Chinese developers have collected about $2 billion in upfront cash, against headline totals reaching ~$34 billion (over half of that from a single CSPC/AstraZeneca obesity portfolio deal earlier this year... but the point stands, IMO).

The competition has gotten fierce enough that even very strong programs in this landscape are struggling to find a home. American biotech Viking Therapeutics’ VK2735, a GLP-1/GIP “me-better” in the mold of tirzepatide, is now in Phase 3 trials, having posted up to 14.7% weight loss in Phase 2 -- and it still has absolutely no big-pharma buyer; by far the most advanced obesity program not yet snapped up. After all, if you’re a pharma -- why overpay for a program like this, when you can get it for a fraction of the cost in China? I digress.

But writing the whole sector off as purely imitative would be inaccurate, comforting though it might be. In some of the newest emerging modalities, specifically the ones the West hasn’t fully mastered yet either, Chinese firms are showing spectacular technical sophistication, and arguably advancing the state of the art in drug design.

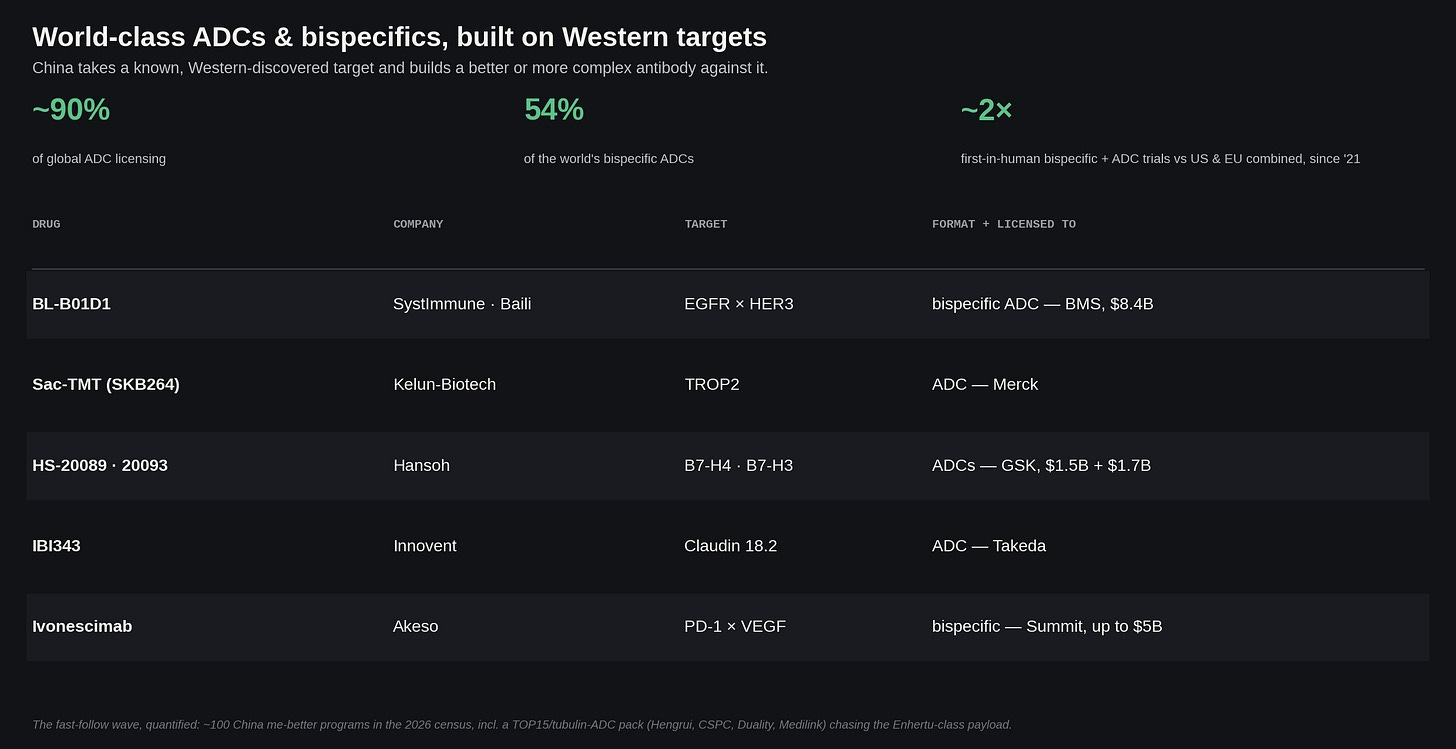

The clearest case of this is the ADC and bispecific wave. China now accounts for something like 90% of global ADC licensing, more than half the world's bispecific ADCs by approvals, and it is running roughly twice as many first-in-human bispecific-and-ADC trials as the US and EU combined since 2021. The poster child of these programs is, of course, ivonescimab, -- Akeso’s PD-1×VEGF bispecific. In the HARMONi-2 trial that read out in 2024, it became the first drug to beat Keytruda head-to-head in lung cancer: managing 11.1 months progression-free survival versus 5.8, a hazard ratio of 0.51. That blowout data print had many industry observers calling it biotech's “DeepSeek moment”.

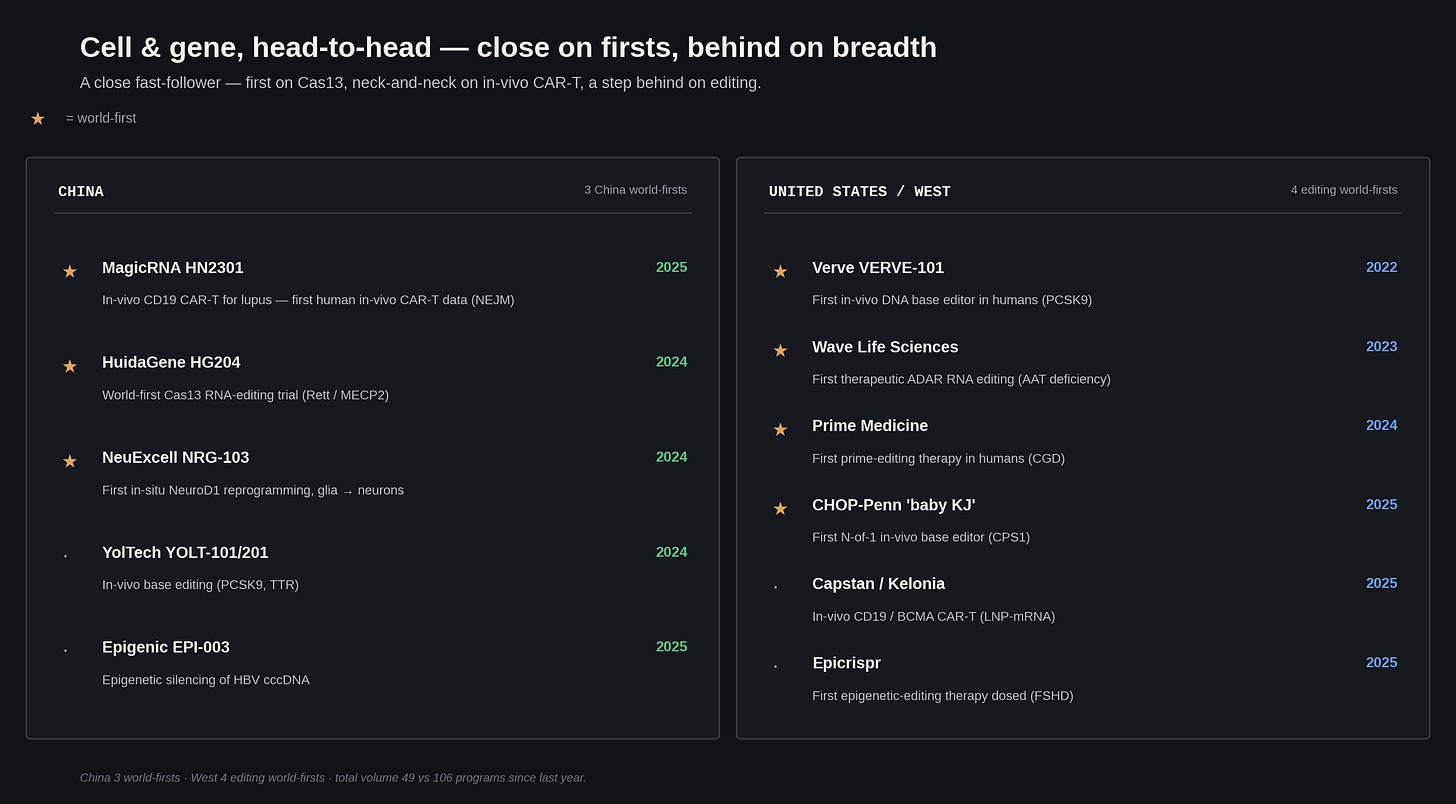

Then there is cell and gene therapy. This is a field where China is advanced enough that I honestly can’t easily nitpick who did what first. Chinese capabilities in both are rapidly approaching parity with the West: recent milestones include a world-first in-vivo CAR-T therapy for lupus, and a first-in-human trial for Cas13 RNA editing; both truly impressive leaps in these notoriously difficult therapeutic paradigms.

The one place I could say that China still trails here is breadth of distinct programs: across cell and gene therapy, I could only find 49 active, unique clinical programs in China — compared to the West’s 106 (even though China runs more than half the world’s CAR-T trials).2

Two kinds of “new”

So maybe it’s time to pack your bags for Shanghai, right?! Not so fast -- you actually might want to hold off on booking that flight.

If I have one complaint about the current discourse on the Chinese biotech miracle, it's the tendency to treat "novelty" as a single variable; which makes it annoyingly difficult to objectively study what's actually happening in reality behind all the chatter. From my viewpoint, there are two completely different flavors of “novelty” semantically at play here, and China is currently dominating one while remaining a mildly enthusiastic spectator in the other.

The first flavor is “target novelty” -- as in: a truly new piece of biology, some mechanism that nobody in the world has successfully drugged before. On this axis, the Chinese biotech sector is definitively playing follow-the-leader. Only about 19% of China's clinical pipeline counts as "first-in-class" under the NMPA's own regulatory definition, which in itself is somewhat overstated, because it just requires that no drug of that class be approved anywhere yet. Western firms can be ahead of a Chinese program in trials on the same target, and it would still be identified as "innovative" by China.

The second flavor of novelty is format, and China's lead here is far more apparent to the naked eye. As alluded to before, China leads engineered-antibody and cell-therapy formats -- making up roughly 70% of global ADC development, ~60% of bispecific/multispecific antibodies, and just over half of registrational CAR-T trials by volume. Meanwhile, the West has retreated to defending its lead in next-generation antibody platforms, targeted protein degraders, radioligands, and mRNA clinical development.

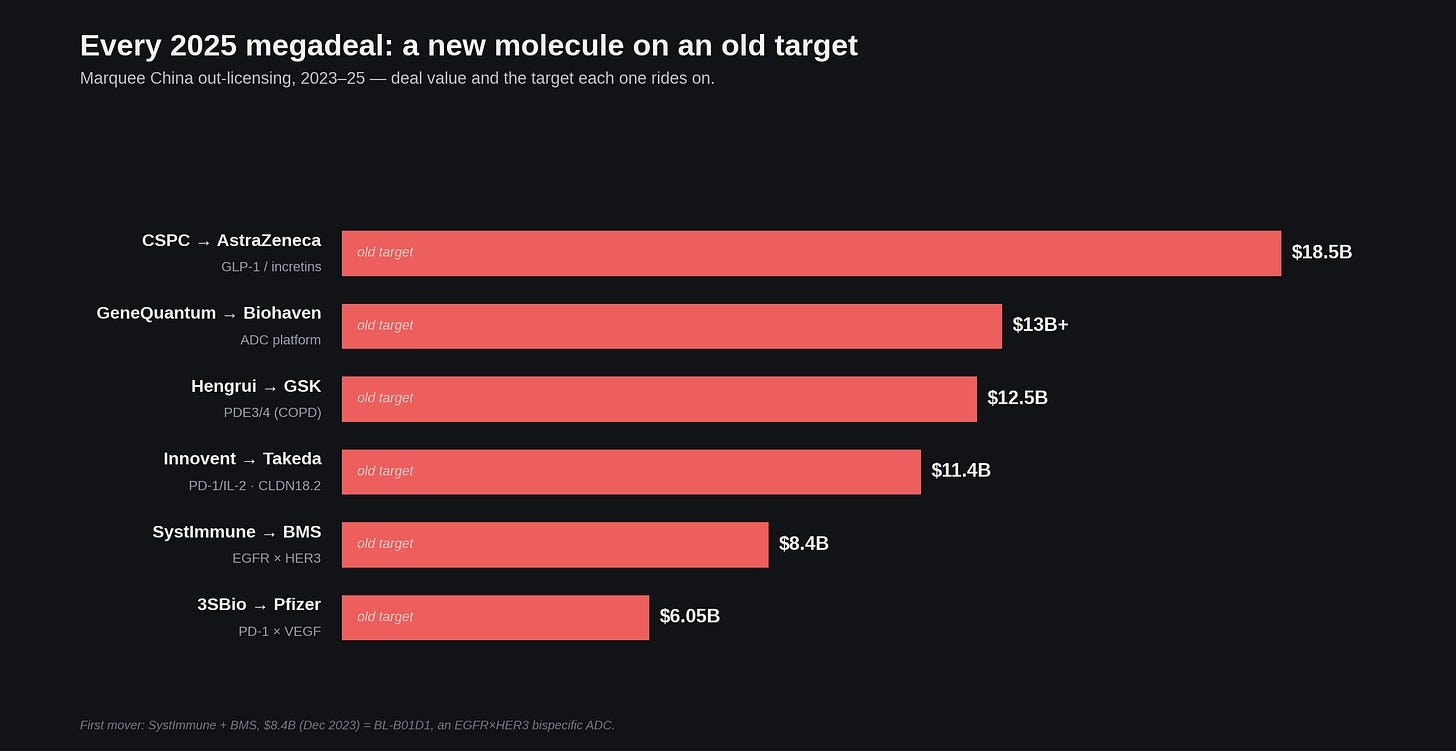

Once you realize that a drug can be "new" in format without being "new" in target, the deal headlines of the past year and a half start to make a lot more sense. Take a look at 2025’s biggest China out-licenses -- practically all of these supposedly groundbreaking molecules are just very clever fast-follows on well-worn biological targets. CSPC/AstraZeneca, GeneQuantum/Biohaven, Hengrui/GSK, Innovent/Takeda, and Systimmune/BMS all ride targets the West discovered and drugged years ago.

But suppose we look a little closer at that impressive list of Chinese ADCs and bispecific antibodies. I invite you to spot a unifying theme…

The truth is, many of these programs are "innovative", but mostly in the sense of taking two things the West invented and supergluing them together. Ivonescimab’s specific embodiment -- a PD-1 arm plus a VEGF arm -- is novel, yet we have known about both targets, and had approved drugs on them, for a very long time. Are these programs interesting? Yes! I am perfectly willing to concede that. I just doubt Chinese researchers would have ever built them if Western pioneers hadn't already mapped out the underlying biology.

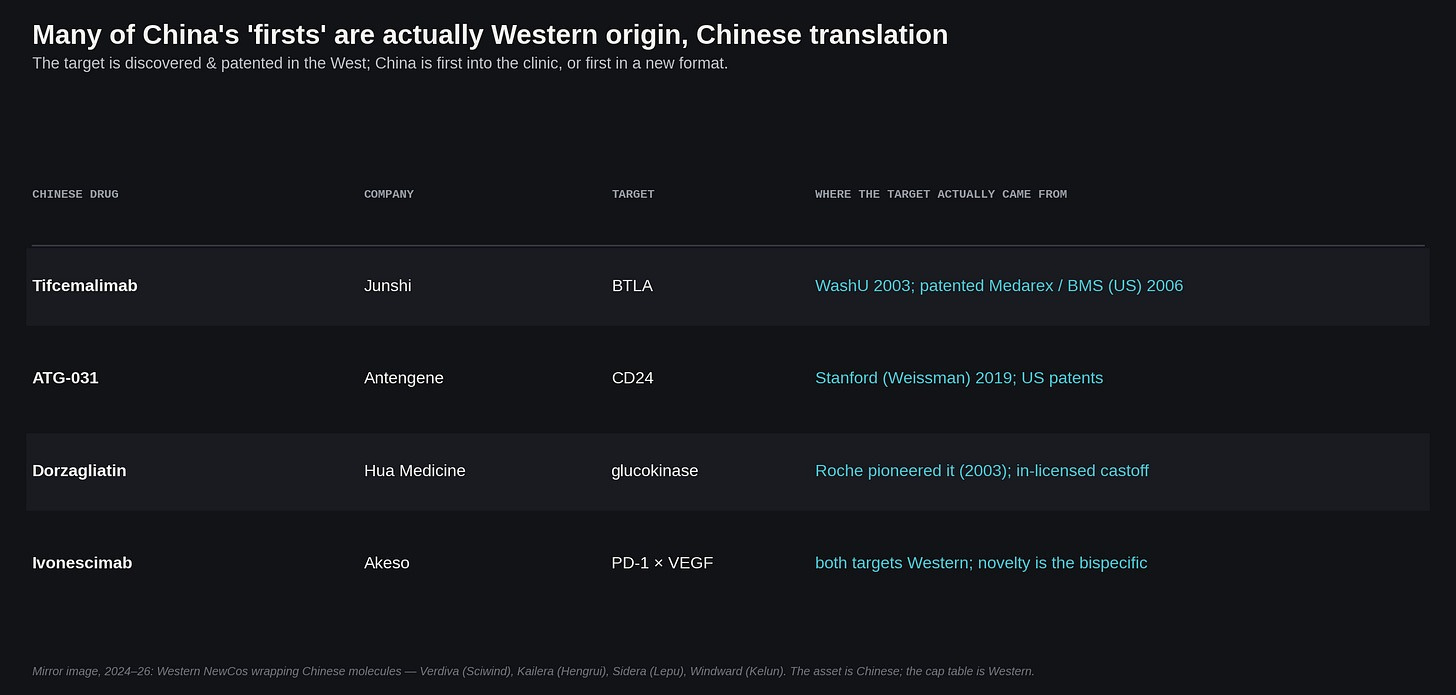

Even when a Chinese company proudly slaps a "first-in-world" sticker on their new drug, they almost always turn out to have been preceded somewhere else. Junshi’s tifcemalimab hits BTLA, which was characterized at WashU in 2003 and patented by Medarex/BMS. Antengene’s ATG-031 hits CD24, out of Weissman’s Stanford lab in 2019. Hua Medicine’s dorzagliatin targets glucokinase, which Roche pioneered in 2003, abandoned, and outlicsensed to… Hua Medicine.

And if you go one level up -- to the paradigms that made these drugs themselves even remotely possible -- you can see that China originated exactly zero of the fifteen founding paradigms. PD-1 came out of Tasuku Honjo’s lab in Kyoto; CAR-T from Zelig Eshhar in Israel; ADCs and PROTACs out of the US; bispecifics and Claudin18.2 out of Germany; the incretin biology behind GLP-1s out of the US and Denmark. That, of course, is a statement about the historical record -- not an indictment for what Chinese academia can and cannot do! But it is still telling that every modality China now dominates in development traces its founding invention somewhere else.

This rhymes with the panic I opened on. The last time America feared an Asian challenger in biotech, the basic science was a part that nobody seriously bothered to contest. The 1984 OTA report that named Japan a major up and coming threat also treated the United States’ commanding position in molecular biology as an absolute given -- instead spending its worry entirely on who would scale and sell what America discovered. China’s current ascent can be argued too to be of that milieu.

At the level of actual programs, the gap is massive. I screened the 2025-26 CDE acceptance lists, 5,565 new-drug filings and 3,128 of them Class-1 "innovative" INDs, against a target census built from ChEMBL and Open Targets, then chased every novel-target claim back to its discovery. On first-in-class clinical entries, the West leads 127 to China’s 21. And if you tighten the screws to only include targets whose biology was first characterized in China, the list dramatically slims down to a pair. One is CD3L1, an immune checkpoint out of Fudan University, now in Phase 1 as BioTroy's BT02. The other is CREPT, out of Tsinghua, also in early-stage trials. Every other "first-in-class" Chinese drug I could track relies on a target that Western scientists discovered, published, or drugged first.

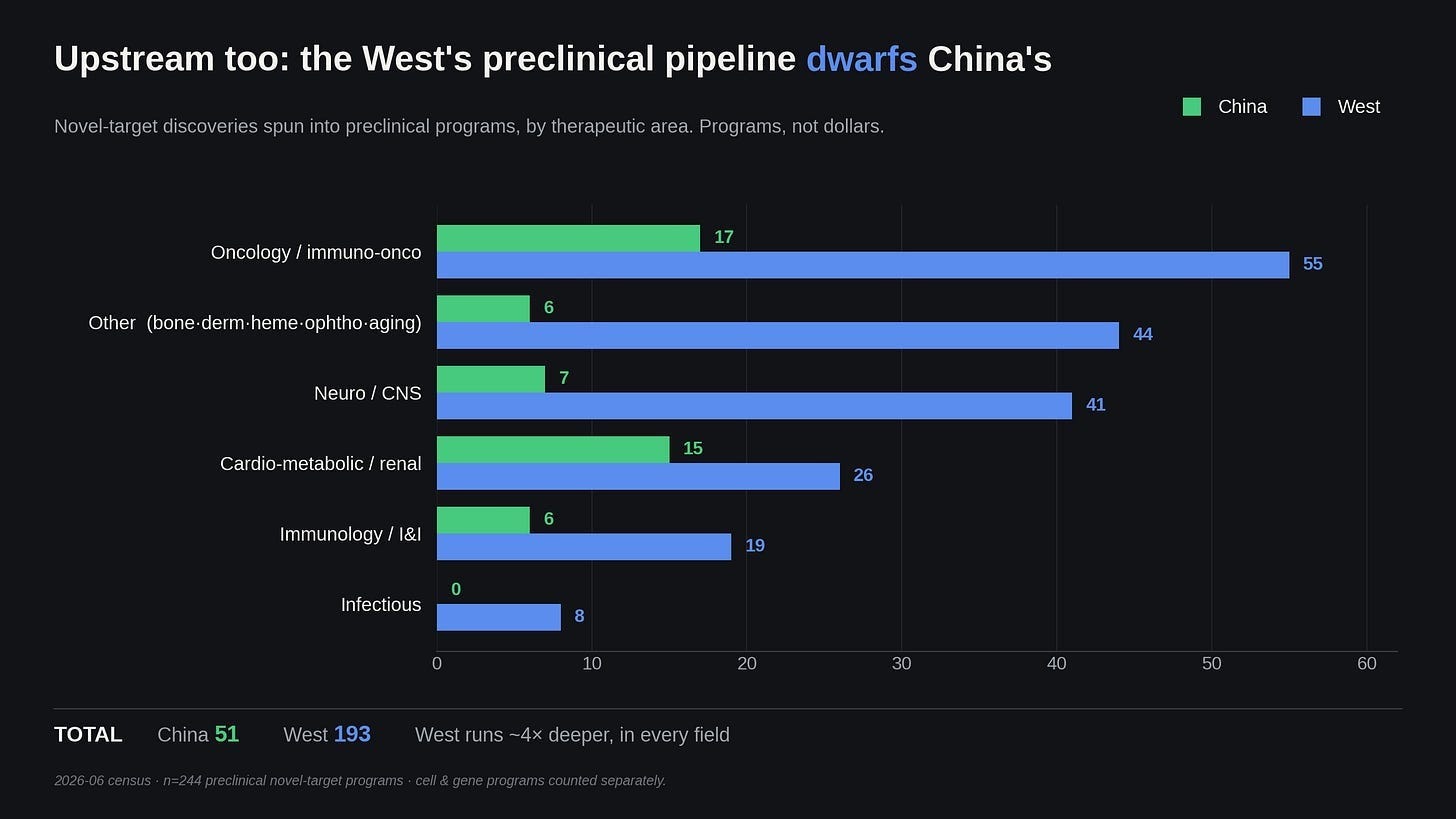

At the preclinical stage, counting only programs with a published discovery behind them, the West leads on novel targets 71 to 41, roughly two to one. China’s 41 are recent, and almost none of the papers predate 2023; most of this new work is instead clustered in two areas. In immuno oncology, Chinese groups have nominated a set of newly discovered tumor checkpoints -- CD48, BTN2A2, LTBR -- each with mouse data showing synergy with anti-PD-1. In metabolic biology, new literature from China has described previously unknown circulating hormones, including “cholesin”, a cholesterol-sensing gut hormone, and “feimin”, a feeding-induced myokine; both discovered by the same lab in 2025.

Looking at this early-stage data, it seems entirely fair to argue that Chinese academic labs are legitimately starting to catch up on the sort of foundational biology that eventually translates into genuinely innovative medicines.

What’s harder for me to conclusively resolve is whether any of this will reach the magnitude of CAR-T or CRISPR. Since practically none of these papers existed before 2023, we are going to be waiting a long time to see the return on investment from them. But judging by the current landscape, the front end of the Chinese biotech pipeline needs more than just a handful of high-impact papers detailing novel mechanisms. Their patent system is a bureaucratic mess, because everything derived from government-funded research are still legally classified as State-Owned Assets. They've tried to fix this, passing their own equivalent of the Bayh-Dole Act years ago to give universities title to patents from government-funded research. But a Chinese public university is itself a state entity, so those patents stay classified as state-owned assets. Disposing of one requires explicit sign-off from several layers of bureaucracy, and an administrator who prices it too low can be held personally responsible for the loss of state property.

Even during a wave of reforms between 2023 and 2025, the national intellectual property administration screened 1.35 million university patents, flagged 680,000 as commercially viable, and then literally hand-matched them to 460,000 specific companies. This brute-force effort tripled the university conversion rate to 10.1% by the end of last year, but having government officials manually assign patents to corporations is probably not the optimal way to handle tech transfer. So even with a centrally coordinated campaign, Chinese universities are still leaving nine out of ten patents untouched!

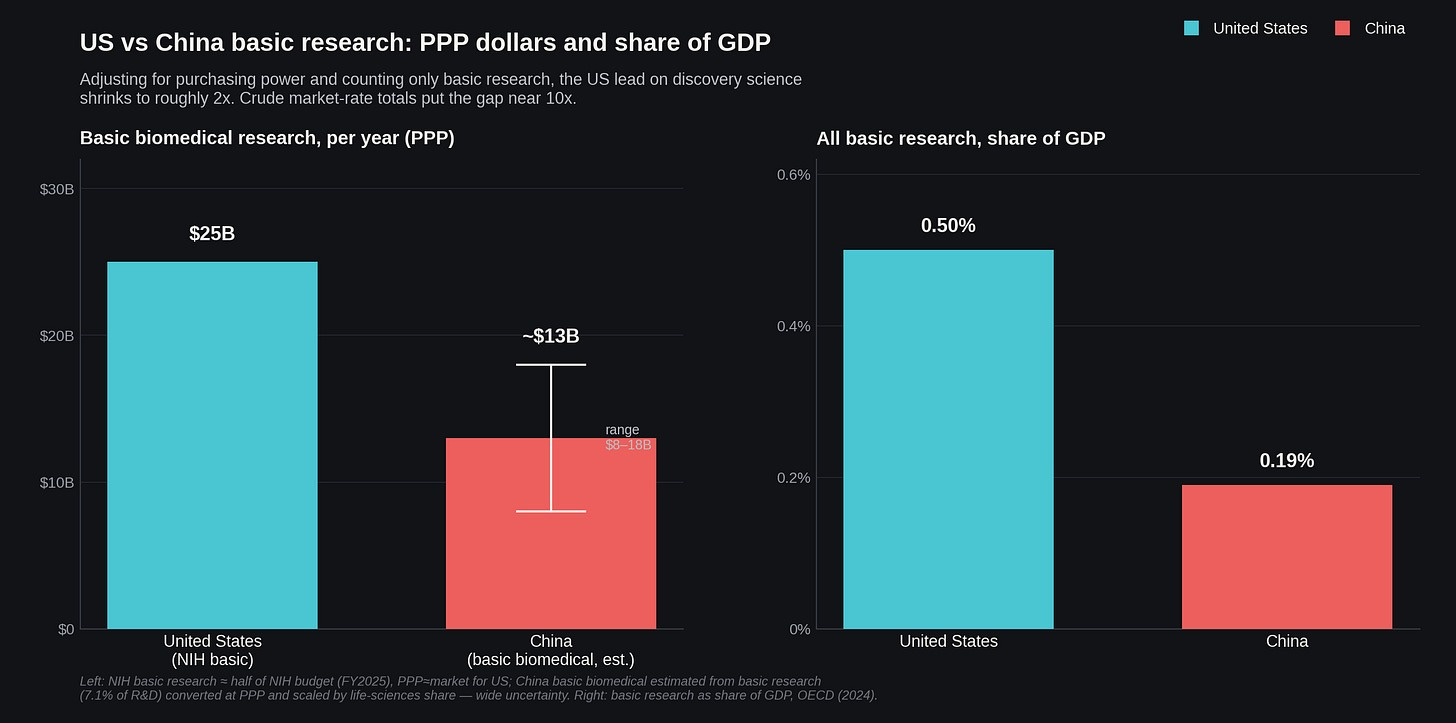

Compare this to the US, where tech-transfer offices and early-stage venture capital have spent decades evolving in symbiosis with universities to turn academic papers into startups. It probably also helps that the US still spends about $25 billion a year on basic biomedical research in purchasing power parity terms, compared to China’s roughly $13 billion3. That means the US is spending 0.50% of its GDP on basic research compared to China’s 0.19%, and that kind of massive funding advantage reliably buys paradigm-level invention on a lag of several years. But even if China eventually closes the spending gap, they still have an execution problem. Until they build a risk-tolerant commercialization ecosystem that can actually capitalize on the science they are already funding, their expanding library of preclinical biology risks being stuck on the shelves of the ivory tower, gathering dust.

Have we run this movie before?

I open this piece on Japan because it's important precedent for the current moment, and weirdly one that everyone conveniently forgets. But at second glance -- how good of a precedent is it, really?

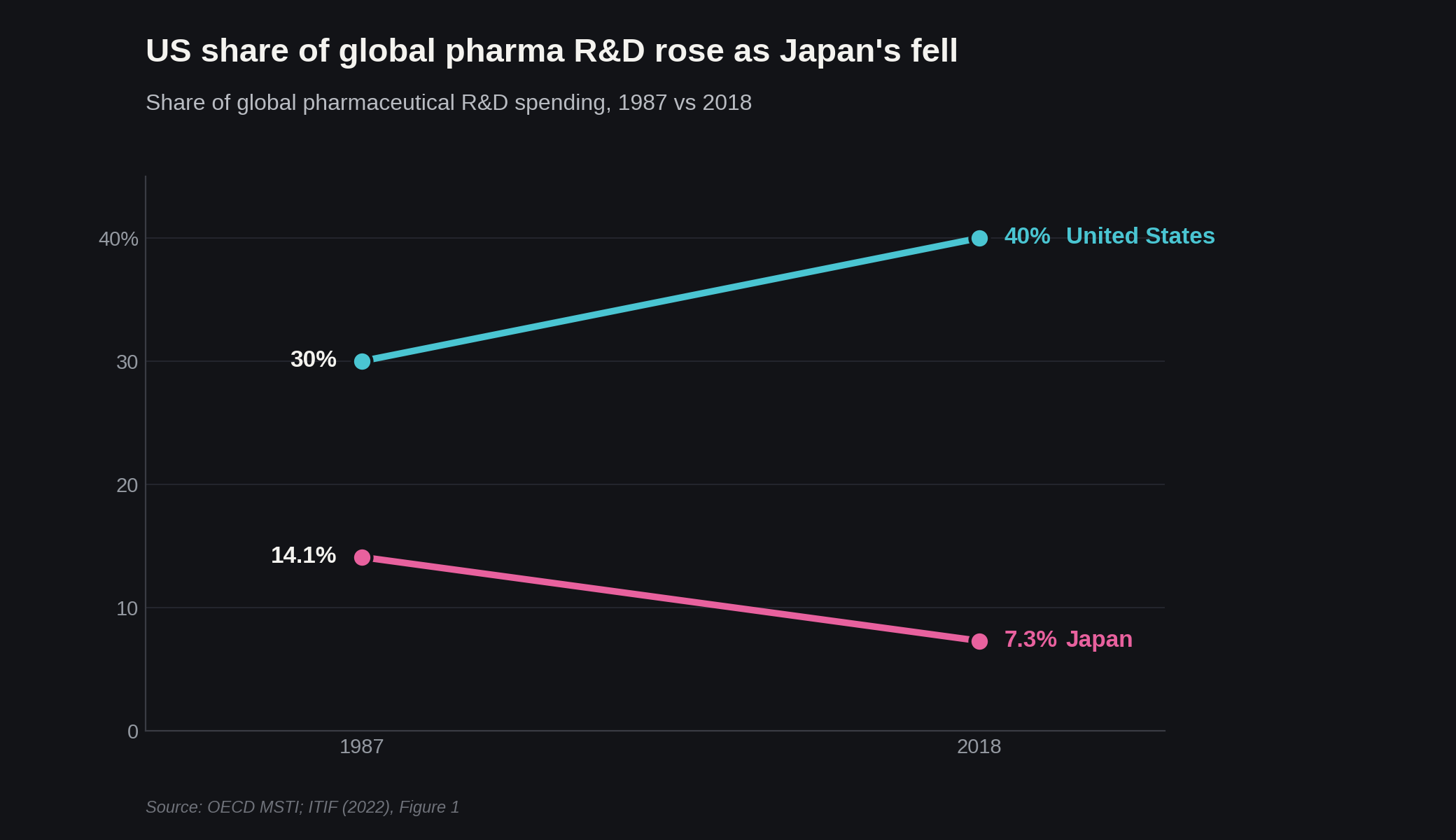

Here's the TL;DR: the Japanese threat fizzled because strong domestic manufacturing and state backing can't beat the West on their own. It had no venture ecosystem to build on this internal boom; meanwhile, all commercial activity in the Japanese biotech sector was stuck between a rock and a hard place, bottled up inside ginormous keiretsu firms, which ended up backfiring by hoarding precious university talent and IP (instead of being spun out into startups). Its national insurance system compounded the problem, pricing new drugs against the existing comparator and revising those prices downward year after year, so the return on a real breakthrough was never much better than on a safe me-too. All of this together is exactly how Japan’s pharmaceutical industry lost its early edge. That didn’t have to be the case! Japan had the science base and the first-in-class track record, some of which I already mentioned in the intro. But because it never properly built out proper commercial rails that can turn a newly approved drug into a global franchise, the sector slowly devolved into producing very good me-toos and little more than that. Its share of global pharmaceutical value-added, consequently, went through a precipitous decline as the country fell into its lost decades -- dropping a sobering 70% between 1995 and 2018. Even by 1999, the US was filing ten times as many biotech patents.

Japan’s two winning cards are the two China holds today, and neither was enough. What about Europe?

You can't blame Europe's loss on a sudden inability to do science. Up through the 1970s, they were essentially the pharmacy for the entire planet. The European Commission actually tracked their own decline in real time: a 1994 competitiveness report noted that while European labs developed half of all new medicines twenty years prior, they had dropped to about a third by the early nineties; effectively concluding it was hard to escape the reality that the US had become the main base for pharmaceutical R&D. And they were entirely right. By 2004, two-thirds of the thirty best-selling drugs globally were American. If you look at the top fifteen pharmas, US firms went from owning less than half in 1989 to over 80% just ten years later.

The thing I find equally sad and funny is that Europe kept inventing new molecules the whole time during this period of quasi-decline. If you just count raw new chemical entities, European labs actually held a plurality from 1993 straight through to 2003, beating the US! What Europe instead lost was their specific slice of the pie that actually makes money: that being from first-in-class drugs, creation of new biotechs, and the privilege of being the first launch market. Basic science stayed in Europe, with a bunch of commercial value irreversibly migrating across the Atlantic because the US was building up an entire ecosystem around financially rewarding science in a way that Europe couldn’t match. We had the NIH funding basic research at a scale no European state could afford, the Bayh-Dole Act letting universities spin discoveries into actual companies, a venture capital sector and a NASDAQ perfectly happy to IPO a biotech firm with zero approved products, and a free-market pricing system that actually rewarded all that insane risk. Europe just had a fragmented mess of a dozen national health systems and pricing regimes, which meant there was nowhere to smoothly launch a new drug.

So Japan had world-class manufacturing and coordinated state backing, and they lost. Europe had the historical scientific pedigree and the raw chemical output, and they lost too. In both cases, the deciding factor came down to who controlled the market where the drugs actually get paid for, and who possessed the financial and regulatory apparatus to carry a raw molecule all the way to a global launch.

The US pays for the world’s drugs

Let’s suppose the science gap keeps closing, which is entirely possible. There is a second ace the US holds, and one China hasn’t figured out how to cross: a highly lucrative market of patients that pays for a lion’s share of the world’s new and innovative drugs.

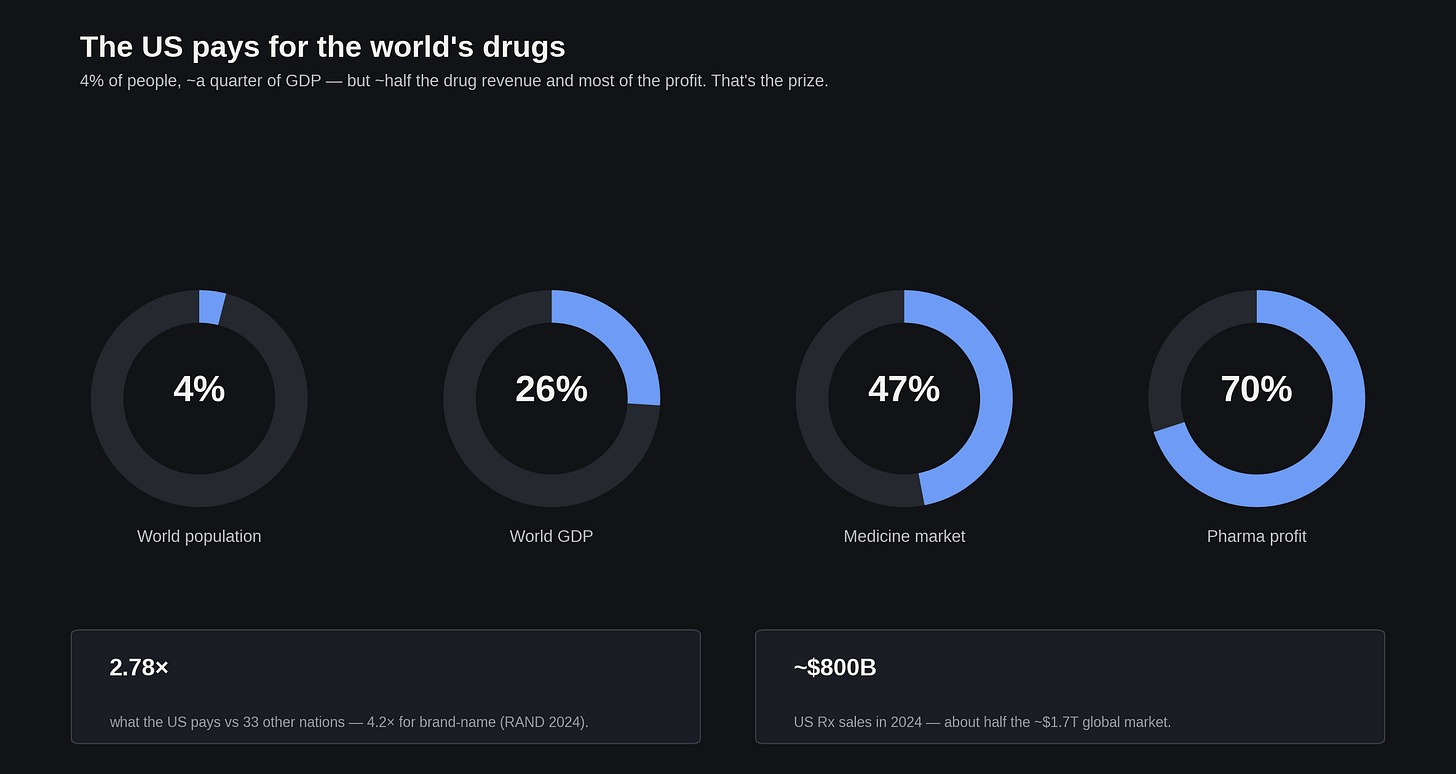

It’s no secret that despite making up 4% of the world’s population, the US produces a quarter of its GDP and roughly three-quarters of the global drug market’s profits. The American market is the prize every pharma company fights over! That is why the whole job of turning an approved molecule into a global franchise, all the way up to managing payers and launches across dozens of countries, rests on infrastructure built around serving patients in the United States. China, on the other hand, hardly has any of this infrastructure (yet).

This lack of commercial reach creates an interesting kind of geopolitical quagmire for China, especially when it comes to the "me-better" drugs they’re heavily concentrated in developing. Historically in pharma, the me-better usually wins. Lipitor was the fifth statin to hit the market, but it became the best-selling drug in history. Humira launched years after the first anti-TNFs, and outsold everyone! Since Chinese firms now do a lot of the engineering and early clinical development, dominating this modern me-better layer, you might expect them to capture most of the value.

But it doesn’t actually play out that way! Those historical me-betters won by conquering the American market using American commercial execution. A modern Chinese me-better can’t reach US patients with domestic data alone; it has to be licensed to a Western pharma giant to run pivotal trials and handle distribution, in order to be kosher for FDA approval. So while these Chinese me-better drugs could eventually outcompete their respective pioneers, the massive US profit margins is going to almost always go to a Western pharma licensee. On the other hand, the Chinese originator will get an upfront payment, some milestone bonuses, and royalties -- real money, no doubt, but a mere fraction of any given program’s total lifetime value.

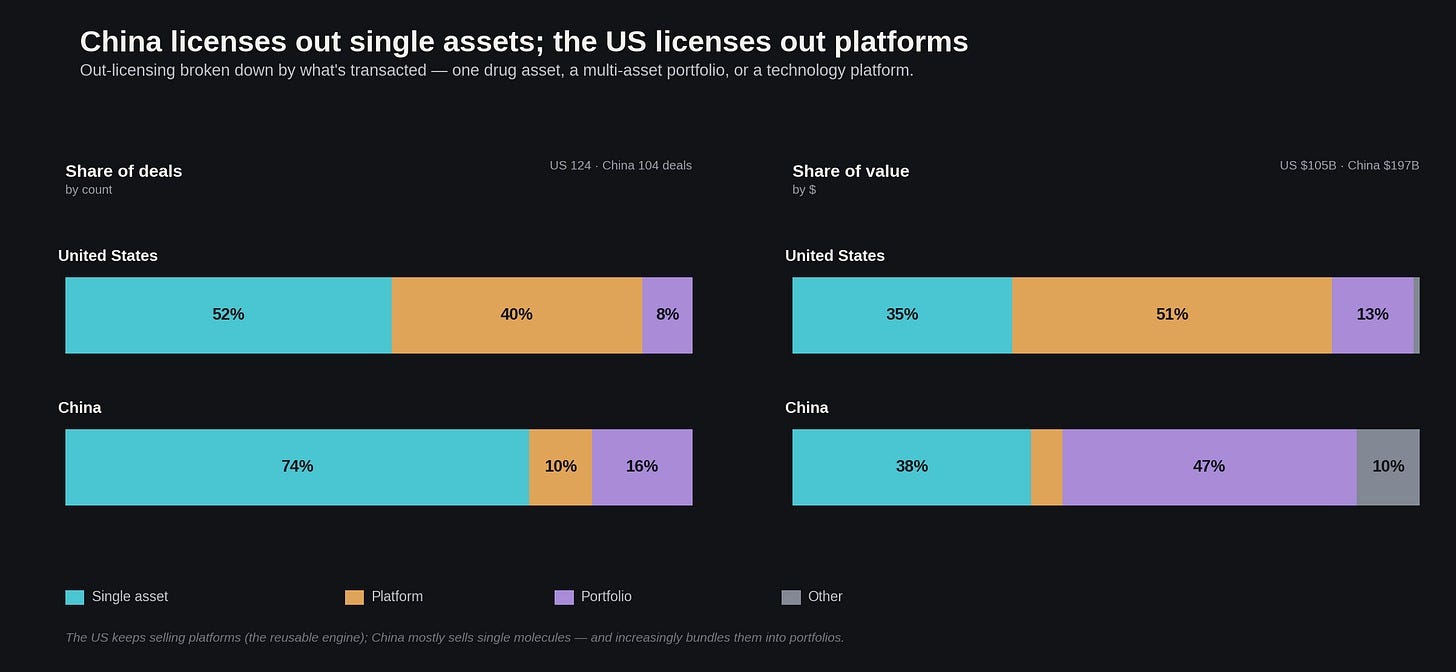

If you look at the granular composition of last year's business development, this dynamic becomes ever the more obvious. While last year’s business development shows US biotech deals split fairly evenly between platforms and single assets, Chinese companies seem far more content to sell off single molecules (though they are increasingly bundling them into portfolios for big pharma). Because they are selling the commercial rights to a specific drug rather than the underlying discovery platform, the upfront payments on these Chinese deals look significantly larger.

Alas, there are cracks beginning to form in that arrangement, of which are well worth addressing. Most infamous of them is the Chinese big pharma BeiGene. Just last year, it successfully renamed itself BeOne Medicines -- and redomiciled to Switzerland to get ahead of potential harms from future geopolitical friction between the West and China. Over the past few years it’s been able to build its own global commercial organization, run multinational trials without a Western contract research organization, which in turn showed that its second-gen BTK inhibitor zanubrutinib (Brukinsa) was superior to AbbVie/J&J’s ibrutinib when tested head-to-head against one another. Brukinsa is now the US BTK market-share leader, posting $792 million in the first quarter of 2025 alone, up 62% year on year.

So none of this is guaranteed to last forever. If today’s turbulent climate of drug pricing continues into the next decade, with IRA negotiations and MFN threatening stable returns on pharmaceutical R&D -- the US could easily handicap its ability to bankroll the next generation of Ozempics and Keytrudas.

Which way, Western pharma?

How is the broader biotech industry modeling this situation? As far as I can tell, people cluster into three main camps:

Option A. Build a Great Wall

Option B. Keep buying, and let the free market sort it out

Option C. Fix the domestic bottlenecks that are causing us to fall behind in the first place

Spoiler alert: I suspect Camp C is basically correct, and one everyone agrees with in principle. But I want to survey all three, partly because the first two factions make surprisingly strong arguments, and partly because watching them fail is highly instructive.

A. Build a Great Wall

I will freely admit that the wall-builders -- a loose coalition of figures that include Joe Lonsdale, Jason Kelly, and the general BIOSECURE/COINS Act crowd -- start from a premise that is genuinely difficult to refute. If a foreign power manufactures roughly 30% of your active pharmaceutical ingredients, holds a monopoly on 41% of your key starting materials, and provides 27% of the drugs used by your military, that power has its hand resting comfortably on a valve it can close at any time. You do not negotiate your way out of that with a slightly prettier term sheet. Their proposed solution is to simply sever the connection: restrict in-licensing, eliminate the "Green List" expedited reviews for Chinese suppliers, lock patentable discoveries behind trade secret protections, and physically stop American venture capital from funding our primary geopolitical rival.

The wall-builders also point to a direct predation problem that standard economic models of cost competition fail to capture: cases where a Western discovery can simply walk out the door and miraculously reappear in a China- origin development program. Pfizer spent 2022 into 2023 litigating exactly this: it accused two former chemists of taking its oral GLP-1 trade secrets on their way out in 2018 and using them to launch Regor Therapeutics, whose GLP-1 work had just anchored a $1.5 billion Lilly deal. Regor denied all of it and countersued, and the case settled in 2023 on undisclosed terms with no finding either way. A live version is now running in RAS oncology. Revolution Medicines -- which originated the tri-complex "molecular glue" approach to drugging RAS -- told Erasca in April 2026 that Erasca's pan-RAS glue infringes a RevMed patent, and that a third party misappropriated RevMed trade secrets tied to it. That third party is Joyo Pharmatech, the Chinese biotech Erasca licensed the molecule from. Both are allegations, and neither has been proven. What they show, the wall-builders argue, is that some of what looks like Chinese fast-following could actually be smuggled Western science.

But this is roughly where I get off the bus. If you actually succeed in building this wall, you instantly destroy the NewCo boom that currently is heling enrich U.S. investors, and which helps keep U.S. clinical pipelines in big pharmas fully stocked. You would make the development of U.S.-originated drugs slower and more expensive while fixing absolutely none of the structural advantages that made China cheap in the first place. You generally do not defeat a competitor by legally prohibiting your own companies from purchasing their most cost-effective components. And realistically, the wall is going to leak anyway. The whole NewCo boom of today is such a workaround in practice, only perhaps a bit ahead of schedule; just grab a Chinese asset, drop it in a Delaware or Swiss shell, and poof, now it is an “American” company. So you can put as many deadbolts on the front door as you like; if the asset has a key to the side entrance, your exposure remains exactly the same.

B. Keep buying; let the market decide

Camp B—represented by people like Peter Kolchinsky at RA Capital -- flips the script on this entirely. They argue that the geopolitical leverage actually runs in our direction, for a reason we have discussed before: the United States controls the only pharmaceutical profit pool that anyone in the world actually cares about. As long as every Chinese molecule eventually has to be handed over to a Western company to achieve commercial viability, China is relegated to the role of a mere supplier, and we get to dictate the terms. Who in their right mind would intentionally destroy a system where they can control the lucrative commercialization phase while heavily discounted molecules just keep magically appearing on your doorstep?! In a very good recent essay, Kolchinsky argues that walling off China will simply cause those assets to reroute to Europe, leaving American patients waiting longer for inferior medications. I agree that this seems entirely plausible.

My only gripe is the word “forever.” Camp B is betting that the US profit pool will stay a moat, and that is not a sure thing. There are more BeOnes waiting in the wings; the moment a single Chinese firm successfully builds its own global commercial infrastructure, you have to start wondering how long the "China handles the engineering and we handle the sales" equilibrium could actually survive -- and whether they will stop at merely selling their humble, organically grown kinase inhibitors (spoiler: they won’t). Beyond that, the phrase "let the market decide" is doing an incredible amount of heavy lifting here, considering that the opposing market is currently running on a combination of artificially cheap state loans, free real estate, and heavily subsidized labor. It is a very strange sort of free market that requires competing against a sovereign wealth fund.

C. Fix our issues at home

It should not surprise anyone that this is the consensus favorite, mostly because banning Chinese in-licensing fails to magically shave a single dollar off the cost of an American clinical trial, and handing over the industry's comparative advantage for a bowl of geopolitical lentil stew has predictable results. Running idea-to-Phase-1 on all-US/EU CROs costs three to four times what it costs in China -- and in such an expensive industry where iteration cycles are long between when a program is started and when it becomes profitable, it’s no wonder that China has become such an attractive destination for early stage drug development.

But on the other hand, there is a massive amount of proven, boring-but-highly-effective regulatory plumbing we could be fixing, almost all of which maps cleanly onto the existing pipeline. Willy Chertman and Ruxandra Teslo have already outlined most of the clinical trial reforms in “The Case for Clinical Trial Abundance”, an excellent set of IFP policy memos that you should absolutely read. I am heavily cribbing their framework below, while adding a few extra thoughts on the tax and capital side of the equation:

Discovery -- Genetic Priority Designation. Fast-track drugs with targets that have strong human-genetic causal evidence; given that genetically supported targets reach FDA approval about twice as often as targets that aren't.

Preclinical/IND -- a Clinical Trial Notification pathway. Let an ethics committee clear low-risk early trials and just notify the FDA. Australia has run this for 30 years with no difference in adverse events; it can now get a Phase 1 started in ~1.5 months instead of ~3.5, and is, partly as a result, about 57% cheaper, net-net. This is already written into the FDA’s FY2027 budget as a legislative ask, which is very exciting.

Phase 1 -- decentralized trials + risk-based monitoring. Run early trials in routine care and monitor by risk instead of painfully verifying every single data point. RECOVERY did this at ~1/80th the cost of a normal RCT and still rewrote the COVID standard of care.

Phase 2/3 -- platform trials + Project Orbis. Shared control arms, one review that clears a bunch of countries at once. A five-arm platform trial needs about 45% fewer patients than five separate two-arm trials -- with I-SPY 2 and REMAP-CAP having shown such a model can work in cancer and critical care. Another initiative by FDA, Project Orbis, successfully cleared 81 drugs across countries by 2024 -- in parallel rather than in agonizing sequence.

Market -- matching China’s innovation-tax playbook. Creating a 'patent box' for drug patents and granting 150-200% super-deductions post-approval can help keep early-stage R&D costs under control, even as IRA and MFN squeeze the revenue pool which keep the lights on. China itself runs a 15% “High & New Tech” corporate rate against a 25% standard. This, in my view, is one of the cleanest ways to sidestep the ongoing pricing fights while they continue.

Capital -- tradable NOLs + R&D credits. Let pre-revenue biotechs sell their unused losses for non-dilutive cash. New Jersey has been doing this since 1999, and companies in the program survive at roughly twice the rate of ones that don't participate; and the state nets ~$2 in tax revenue per $1 of credit.

So how screwed are we?

We aren’t screwed yet.

The US still controls the two most important nodes in leading the biotech industry development: we have an academic pipeline that turns yoghurt bacteria into CRISPR, and the commercial machine that can turn an approval letter emailed out of a building in Silver Spring into a global franchise.

China doesn’t really possess those capabilities -- yet. Their basic research output is largely siloed within academic institutions, and their ability to commercialize drugs globally is nearly nonexistent, despite them actively trying to change that. What they do have is a massive and growing chunk of the intermediate steps of creating a new drug -- first with contract manufacturing, and now with early clinical development -- built to a scale that a previous disruptor like Japan was never quite able to pull off. But historically speaking, the middle is not the part of the supply chain that actually dictates terms.

If America loses its current advantage, it will probably be an unforced error born of domestic mismanagement rather than a case of China simply out-subsidizing us. If we allow price controls and legislative battles to crush expected commercial returns, our domestic R&D ecosystem could be at serious risk of drying up -- leading us to go the way of Europe. Alternatively, if American biotechs just default to exclusively doing cheap in-licensing of foreign assets, American capital stops funding domestic translational medicine. This is exactly how Europe managed to maintain perfectly good basic science while watching all the actual commercial value cross the Atlantic. If we can manage to do some boring regulatory spring cleaning now, while the system is still mostly fixable, China will probably remain a useful middleman in the relay race that is drug development. Otherwise, we will end up running a high-stakes test of whether the fall of American biotech will look more like that of the semiconductor industry or the steel industry.

For those curious - you can check my math & methodology for these program’s development costs here.

Trial count for C> is heavily swollen by single-site hospital studies; I’m counting program counts for assets headed to a global finish line -- and here, the West’s pipeline is still bigger.

US NIH basic research is taken as ~half of NIH’s ~$47B FY2025 program level (CRS), giving ~$25B; PPP ~~ market for US.

China’s 2024 basic research is ¥249.7B, which NBS reports as 6.91% of their ¥3.61T total R&D spent that year; PPP-converted to ~$54B and scaled to life-sciences share (~20-25%) for ~$13B in basic biomedical R&D. $8-18B band spanning market-rate-to-PPP conversion & life-sciences share.

Extremely comprehensive overview. I tend to agree with you Alex on the options. The US has to address its internal issues first (as you alluded), and their are clear signs that the FDA is moving in the right direction (perhaps not fast enough for some). But that will still be insufficient to address the API challenges which can only be corrected by the US government providing minimum order guarantees for indigenous manufacturing of critical drugs (mostly generic).

My concern would be along the lines that there is no evidence that China will not ascend the value chain over time (as it has in many other industries) with the construction of genuine integrated international drug companies. In the first instance Europe looks vulnerable for such "encroachment" given its low growth, high debt and challenges in spending more on defence.

But perhaps I'm being too cynical in viewing this in such zero sum terms. After all if patients can be treated with effective drugs that were previously out of reach, that should be viewed as unequivocally positive. Right?